India Data Center Market: By hardware (Servers (Blade servers, Rack servers, Tower servers, Micro servers), Storage Systems (Storage Area Network (SAN), Network-Attached Storage (NAS), Direct-Attached Storage (DAS), Cloud storage), Power and Cooling Systems (Power Supply, Uninterruptible Power Supply (UPS) systems, Generators, Power distribution units (PDUs), Cooling Solutions, Air conditioning units, Liquid Cooling Systems, Advanced Cooling Technologies), Racks and Enclosures (Open frame racks, Enclosed Racks, Customized Enclosures); End Users (IT and Telecom, Banking, Financial Services, and Insurance (BFSI), Healthcare, Government, Manufacturing, and Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 12-Jan-2026 | | Report ID: AA0724871

Market Scenario

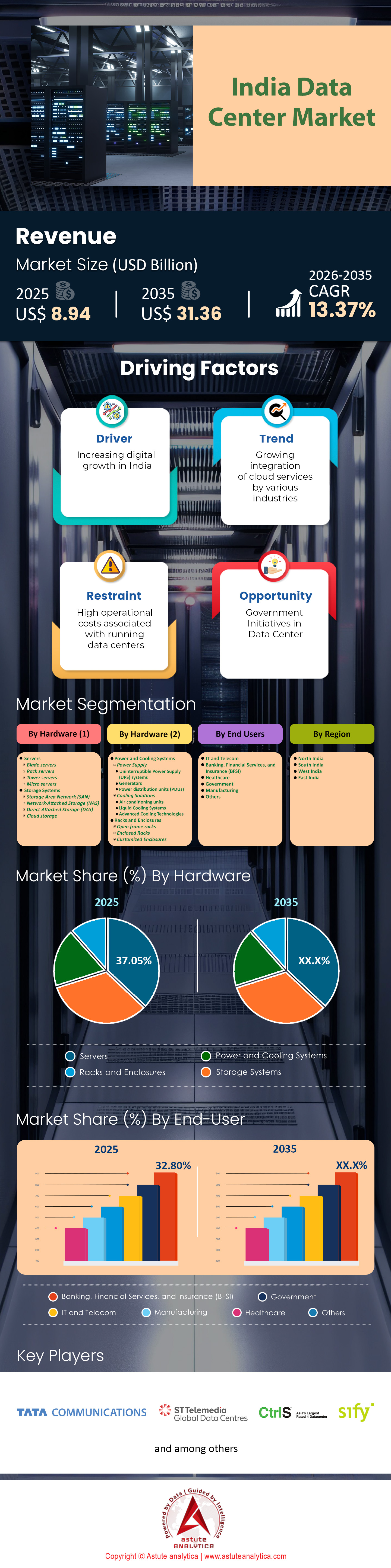

India data center market was valued at US$ 8.94 billion in 2025 and is projected to hit the market valuation of US$ 31.36 billion by 2035 at a CAGR of 13.37% during the forecast period 2026–2035.

The global digital economy is witnessing a seismic shift, and India has firmly positioned itself at the epicenter of this transformation. As we navigate through 2026, the India data center market has evolved from a burgeoning sector into a critical pillar of the global internet infrastructure. Fuelled by the explosive adoption of Artificial Intelligence (AI), robust 5G penetration, and aggressive government digitalization mandates, the market is expanding at a velocity that outpaces most mature economies.

Key Findings

- Based on hardware, servers accounted for more than 37.05% of the total revenue in the India market

- Based on end users, Banking Financial Services and Insurance (BFSI) sector is the biggest end users with over 32.80% market share.

- West India capture over 44% market share.

- India data center market is expected to grow at CAGR of 13.37%

How Massive is the Current Operational Footprint of Data Center in India?

The year 2025 was a watershed moment for capacity addition. According to recent industry data from Savills and JLL, India’s operational data center stock surged to approximately 1,520 MW by the close of 2025. This was driven by a record-breaking supply addition of 387 MW in a single year, significantly overshadowing the 191 MW added in 2024. This rapid acceleration indicates that developers are racing against time to bridge the demand-supply gap.

Geographically, the India data center market remains highly concentrated yet is showing signs of diversification. Mumbai continues to reign supreme, commanding over 52% of the total installed capacity. The city’s dominance is anchored by its status as a submarine cable landing hub and its reliable power grid. However, Chennai is cementing its position as the second-largest hub with nearly 20% market share, driven by new cable landings like MIST. Meanwhile, Delhi-NCR and Hyderabad are emerging aggressively, with Hyderabad attracting hyperscalers due to its disaster-safe geography and proactive state policies.

To Get more Insights, Request A Free Sample

Who Are the Titans Steering the Ship?

The competitive landscape of the India data center market is fierce, characterized by a mix of domestic conglomerates and global heavyweights. STT GDC India remains a market leader, managing a massive portfolio with over 300 MW of critical IT load. However, the challenger mindset is evident in AdaniConneX—a joint venture between Adani Enterprises and EdgeConneX—which has set an audacious target of 1 GW (1,000 MW) capacity. Their aggressive strategy is backed by a USD 10 billion investment roadmap.

NTT reported nearly 300 MW (precisely 292 MW) of live IT load in July 2025, with aggressive expansions underway, including plans to reach 400 MW within 18-24 months via new campuses in Noida, Hyderabad, and Bengaluru. Earlier claims of "more than 265 MW" date to 2023-2024 launches. Meanwhile, CtrlS Datacenters has committed USD 2 billion for expansion over the next few years, focusing on green, AI-ready campuses. The market is also seeing tech giants stepping in directly; for instance, Yotta Data Services has pivoted from traditional colocation to becoming an AI-cloud powerhouse, procuring 16,000 Nvidia H100 GPUs to service high-performance computing needs.

What Mega-Projects are Redefining the Skyline?

The pipeline for ongoing and upcoming projects is staggering across the India data center market. Industry reports indicate that 1.03 GW of colocation capacity is currently under construction for the 2024–2028 period. Beyond this, an additional 1.29 GW is in the planning stage, ensuring a steady supply of inventory.

One of the most widely discussed developments is the AdaniConneX and Google partnership, focusing on a facility in Vizag with a potential ecosystem investment of USD 15 billion. Similarly, Microsoft has acquired a 48-acre land parcel in Hyderabad for USD 32 million, signaling the start of a massive hyperscale campus. In the renewable space, CtrlS is constructing a 125 MWp solar farm to power its upcoming facilities, reflecting the sector's shift toward self-sustained green campuses.

Why is India the World’s New Digital Hotspot?

Several convergent factors are turning India into a magnet for data center investment. First is the connectivity revolution. The activation of the 2Africa Pearls cable (180 Tbps) and the upcoming India-Asia-Express (IAX) cable (200 Tbps) in 2025 has exponentially increased international bandwidth.

Second is the sheer scale of domestic consumption in the data center market. Cloud Service Providers (CSPs) accounted for 54% of active absorption in 2025, driven by enterprise digitization. Furthermore, India offers a significant cost advantage; the cost to build a MW of capacity in India hovers around USD 4-5 million, compared to USD 8-10 million in developed markets. Combined with a data localization policy that mandates critical data to remain within sovereign borders, global enterprises have no choice but to establish a local physical presence.

Where is the India Data Center Market Heading by 2035?

While short-term forecasts by Astute Analytica predict that the market will hit 1.8 GW by 2027, long-term projections are far more bullish. Nomura forecasts that India’s data center capacity could skyrocket to 9.2 GW by 2030. Extrapolating to 2035, industry consensus suggests India could rival European markets, potentially exceeding 12-15 GW if energy infrastructure keeps pace.

Power consumption is the critical variable here in India data center market. With data centers expected to consume 8% of global energy by 2030, India's data center power use is forecast to quadruple from 13-17 TWh in 2024 to 57 TWh by 2030, rising from 0.8-1% to 2.6-3% of national electricity generation. This equates to needing 15-30 GW additional capacity, about 10% of planned renewables.. Consequently, the push for renewable energy is non-negotiable. The government’s target of 500 GW of non-fossil fuel capacity by 2030 is directly aligned with the industry’s need for green power, ensuring that this growth does not derail national climate goals.

Which Facility Sizes Are Winning the Race?

The India data center market is witnessing a clear shift toward Hyperscale data center Campuses. The era of small, fragmented server rooms is over. Facilities with capacities exceeding 50 MW to 100 MW are witnessing the highest growth. This is driven by AI workloads that require high-density racks. For instance, CtrlS has engineered its new buildings to support 135 kW per rack, and Nvidia’s NVL 72 implementations require liquid-cooled racks consuming up to 140 kW.

While hyperscalers dominate volume, Edge Data Centers are seeing strategic growth in Tier-2 cities like Bhopal and Lucknow to support 5G latency requirements. However, in terms of sheer capital deployment and MW capacity, large-format hyperscale parks are indisputably leading the market.

How Are Government Policies Fueling This Combustion in India Data Center Market?

The Government of India has played a pivotal role by granting "Infrastructure Status" to the sector, unlocking easier access to long-term credit. The cabinet’s approval of USD 1.24 billion (₹10,732 crore) for the IndiaAI Mission is a game-changer, aiming to subsidize the deployment of 10,000 GPUs for startups and researchers.

State-level policies are equally aggressive. Andhra Pradesh’s Policy 4.0 eliminates transmission charges for open-access power, effectively reducing operational costs by 20-30%. Similarly, Telangana and Tamil Nadu offer land subsidies and single-window clearances, which has accelerated projects like STT GDC’s USD 229 million expansion in Tamil Nadu. These regulatory tailwinds provide the stability international investors require for long-term capital deployment.

What Trends Are Shaping the Immediate Future?

The most defining trend of 2025-2026 is the "AI-fication" of infrastructure in India data center market. Standard data centers are being retrofitted or built from scratch to accommodate the heat generated by AI chips. The global liquid cooling market, projected to reach USD 31 billion by 2032, is finding early adoption in India, with operators like Yotta and NTT deploying Direct-to-Chip cooling technologies.

Another significant trend is the rise of Green Data Centers. With STT GDC India already achieving 62.5% renewable energy usage, the industry is moving toward a "Green First" approach. Investors like Aurum Equity Partners have launched specific funds, such as a USD 400 million allocation, dedicated solely to green, AI-powered facilities.

Segmental Analysis

By Hardware, AI Compute Demand and PLI Incentives Driving Hardware Revenue Dominance

The hardware segment’s 37.05% revenue share of the India data center market is primarily fueled by the aggressive procurement of AI-ready compute infrastructure and government-backed manufacturing incentives. The surge in Generative AI has compelled data center operators to deploy high-density server fleets at an unprecedented scale. Yotta Data Services exemplifies this capital-intensive shift, having ordered over 16,000 NVIDIA H100 GPUs to power its Shakti Cloud, with plans to scale this inventory to 32,768 units by the end of 2025.[1] This massive capital outlay for GPU-heavy servers directly inflates the hardware segment’s financial footprint.

Concurrently, the Production Linked Incentive (PLI) 2.0 scheme has successfully catalyzed domestic high-value manufacturing, pushing the hardware demand further in the data center market. Netweb Technologies, a key beneficiary, reported a staggering 154.4% year-on-year income growth in Q1 FY25, with its AI systems revenue surging by 146%.[2] Similarly, global giants like Lenovo have localized production in Puducherry to manufacture 50,000 AI rack servers annually, catering to both domestic and export markets. This dual engine—massive import of high-value AI components by operators and a booming domestic server manufacturing ecosystem—validates the hardware segment's commanding revenue dominance.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By End Users, Regulatory Compliance and Digital Scale Forcing Massive BFSI Infrastructure Spend the Highest and Emerge as the Leader Contributor

The BFSI sector’s 32.80% market share in the India data center market is anchored by the immense IT infrastructure required to support India’s exploding digital transaction volumes and stringent data localization mandates. Financial institutions are allocating record budgets to technology to sustain operations. State Bank of India (SBI) increased its tech budget to ₹10,525 crore for FY25, while ICICI Bank reported that technology expenses accounted for approximately 10.7% of its total operating expenses, underscoring the sector's reliance on premium IT infrastructure.

Operational scale is equally critical; HDFC Bank’s "Shift Right" technology transformation is designed to support over 450 million monthly transactions, necessitating a robust hybrid cloud architecture and expanded data center capacity. Beyond voluntary upgrades, the Reserve Bank of India (RBI) strictly enforces data localization, compelling global fintech players and domestic banks to lease significant colocation space within Indian borders. This regulatory compulsion, combined with the exponential growth of UPI transactions, ensures that the BFSI sector remains the primary financier of the Indian data center market, driving sustained demand for secure, high-uptime facilities.

To Understand More About this Research: Request A Free Sample

Country Analysis

Subsea Connectivity and Financial Clusters Cementing Mumbai’s Regional Supremacy

West India’s capture of over 44% market share of the India data center market is overwhelmingly driven by Mumbai’s status as the country’s undisputed connectivity gateway. The region’s dominance is physical: Mumbai hosts the highest concentration of India's 17 international subsea cable systems, including major landing stations for Tata Communications, Airtel, and Reliance Jio. The upcoming 2Africa Pearls cable system, one of the longest in the world, has designated Mumbai as a key landing hub, further solidifying the city's role in routing global data traffic.

This connectivity advantage attracts hyperscale investments that other regions cannot match. STT GDC India is currently constructing two new facilities in Navi Mumbai to meet this demand, while CtrlS Datacenters is expanding its footprint with a 300 MW capacity roadmap, supported by a captive solar farm in Maharashtra. Furthermore, the presence of the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) creates a non-negotiable need for low-latency infrastructure for high-frequency trading firms. This convergence of superior subsea connectivity, reliable power infrastructure, and a captive financial client base makes West India the default destination for mission-critical IT deployment.

Top 5 Recent Developments in India's Data Center Market

- AdaniConneX and Google Partnership (Oct 2025): Adani Enterprises' joint venture AdaniConneX partnered with Google to build India's largest data center campus in Visakhapatnam, Andhra Pradesh, with 1 GW capacity over five years, powered by renewables and featuring subsea cables.

- TCS HyperVault Launch (Nov 2025): Tata Consultancy Services announced HyperVault with TPG's up to $1B investment (Rs 18,000 crore total) for GW-scale AI-ready data centers, offering liquid-cooled, high-density facilities nationwide.

- Reliance Jamnagar Data Center (Jan 2025): Reliance Industries revealed plans for a 1 GW AI data center in Jamnagar, Gujarat—the world's largest—partnering with NVIDIA for chips, aiming to triple India's capacity.

- CtrlS Hyderabad AI Cluster (Jan 2025): CtrlS Datacenters signed an MoU for Rs 10,000 crore investment in a 400 MW AI data center cluster in Hyderabad, announced at WEF Davos.

- Sify Vizag AI Data Center (Oct 2025): Sify broke ground on a 50 MW AI-ready data center and open cable landing station in Visakhapatnam, with USD 168M investment to boost low-latency AI and connectivity

Top Players in India Data Center Market

- Tata Communications Ltd

- STT GDC INDIA Pvt Ltd

- Datacenters Ltd

- Sify Technologies

- Netmagic Solutions Pvt Ltd

- Web Werks India Pvt Ltd

- ESDS Software Solutions Ltd

- NxtGen Datacenter and Cloud Technologies Pvt Ltd

- GPX India Pvt Ltd

- Yotta Data Services Pvt. Ltd

Market Segmentation Overview:

By Hardware

- Servers

- Blade servers

- Rack servers

- Tower servers

- Micro servers

- Storage Systems

- Storage Area Network (SAN)

- Network-Attached Storage (NAS)

- Direct-Attached Storage (DAS)

- Cloud storage

- Power and Cooling Systems

- Power Supply

- Uninterruptible Power Supply (UPS) systems

- Generators

- Power distribution units (PDUs)

- Cooling Solutions

- Air conditioning units

- Liquid Cooling Systems

- Advanced Cooling Technologies

- Power Supply

- Racks and Enclosures

- Open frame racks

- Enclosed Racks

- Customized Enclosures

By End Users

- IT and Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Government

- Manufacturing

- Others

By Region

- North India

- South India

- West India

- East India

FREQUENTLY ASKED QUESTIONS

The market was valued at USD 8.94 billion in 2025 and is projected to skyrocket to USD 31.36 billion by 2035. This expansion represents a robust CAGR of 13.37%, driven by rapid digitalization, 5G rollouts, and the exponential rise of AI-driven workloads.

West India commands over 44% of the market share, with Mumbai holding 52% of total installed capacity due to its subsea cable ecosystem. However, Hyderabad and Chennai are emerging as high-growth alternatives, offering disaster-safe geographies and aggressive government incentives for hyperscale developments.

The BFSI (Banking, Financial Services, and Insurance) sector is the largest end-user, holding a 32.80% market share. Demand is anchored by surging digital transaction volumes, UPI adoption, and strict RBI data localization mandates requiring massive domestic storage and processing infrastructure.

AI adoption has pushed the Servers segment to capture 37.05% of total hardware revenue. Operators are aggressively shifting capital toward high-density computing, exemplified by Yotta’s procurement of 16,000 Nvidia H100 GPUs, necessitating a transition to advanced liquid-cooling systems.

Key leaders include STT GDC India (300 MW+), NTT Global Data Centers, and AdaniConneX. The landscape is witnessing intense competition, highlighted by AdaniConneX’s audacious goal of 1 GW capacity and ecosystem investments exceeding USD 15 billion with partners like Google.

Green energy is critical, as data centers are projected to consume massive power by 2030. With the government targeting 500 GW of renewable energy, players like CtrlS and STT GDC are building captive solar farms to ensure long-term operational viability and ESG compliance.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |