Unmanned Electronic Warfare Market: By Product Type (Unmanned Electronic Warfare Equipment (Jammers, Directed Energy Weapons (DEWs), Software Defined Radio (SDR), Frequency Hopping (FH) Radios, Acoustic Sensors (Microphones), Optical Sensors (Cameras), Antennas / Antenna Arrays, Other Equipment) and Unmanned Electronic Warfare Operational Support); Capability (Electronic Support (ES), Electronic Protection (EP), Electronic Attack (EA)); Platform (Airborne, Ground, Space, Naval); Mode of Operation (Semi-Autonomous and Fully Autonomous); End Users (Government & Defence and Commercial & Industrial); Regional Analysis— Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 04-Jan-2026 | | Report ID: AA1223706

Market Scenario

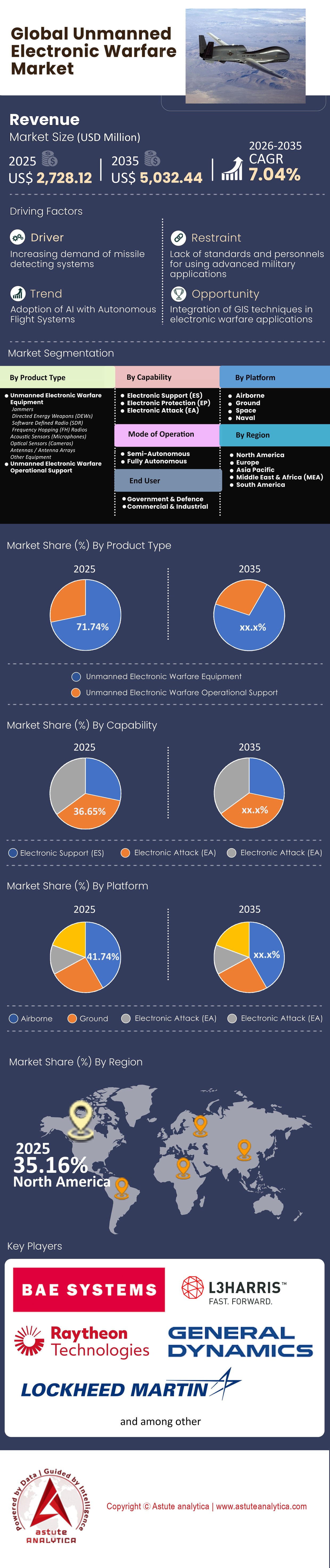

Unmanned electronic warfare market is poised to attain a market valuation of US$ 5,032.44 million by 2035 from US$ 2,728.12 million in 2025 at a CAGR of 7.04% during the forecast period 2026–2035.

Key Findings

- In the product type segment of the global unmanned electronic warfare market, Unmanned Electronic Warfare Equipment emerges as the dominant category. Holding an impressive 71.74% market share.

- In the capability segment, Electronic Protection (EP) holds the highest market share at 36.65%.

- In the platform-based segmentation, the Airborne segment takes the lead with a 41.74% market share in the global unmanned electronic warfare market. The segment is also expected to grow at the highest CAGR of 7.82% during the forecast period.

- In the end-user segment, the government & defence category is leading the global market, holding an overwhelming 86.07% market share and the highest projected CAGR of 7.28%.

- North America holds a commanding position with over 35% of the global market share.

Unmanned Electronic Warfare (EW) represents the integration of electromagnetic spectrum capabilities—jamming, sensing, decoying, and kinetic interception—onto autonomous platforms. Unlike traditional "exquisite" systems that rely on large, manned aircraft or stationary ground vehicles, these solutions utilize distributed, expendable architectures.

The unmanned electronic warfare market is rapidly shifting toward "attritable" systems, which are platforms cheap enough to be lost in combat but capable enough to neutralize high-value threats. Operators manage these systems through software-defined interfaces rather than direct joystick control, allowing a single human to oversee swarm-on-swarm engagements.

To Get more Insights, Request A Free Sample

What Economic Factors Drive the Surge in Demand Across the Global unmanned electronic warfare market?

Cost-exchange ratios currently dictate the procurement strategies of major defense powers. State and non-state actors have exposed a critical vulnerability in traditional air defense: sending cheap drones to deplete expensive interceptors. Data from Ukraine in August 2025 illustrates this disparity, where Ukrainian interceptor drones costing roughly USD 2,500 successfully defeat Russian targets valued between USD 30,000 and USD 50,000. Military planners realize that sustaining a war of attrition requires defensive systems that are financially sustainable.

Saturation tactics further compel this market shift. Russian forces launched a record 818 drones and missiles in a single strike against Ukrainian infrastructure in September 2025. Human operators simply cannot process targets at that volume and speed. Consequently, the unmanned electronic warfare market is driven by the absolute necessity for automated, high-volume responses that manned systems cannot physically provide.

How Are Active Conflicts Shaping Real-World Deployment?

Ongoing wars serve as the primary sandbox for validating and evolving these technologies. The conflict in Ukraine has transitioned into a contest of electromagnetic adaptation. By Summer 2025, Russian forces fielded fiber-optic guided drones immune to traditional radio-frequency jamming. These units extended their operational range to 20 km, and advanced variants appeared in late 2025 with ranges of 50 to 60 km. Such developments forced the unmanned electronic warfare market to pivot from purely soft-kill jammers to kinetic interceptors capable of physical impact.

Maritime operations in the Red Sea provide equally compelling demand signals. Houthi forces executed 16 confirmed attacks on commercial vessels in June 2024 alone. Coalition forces were forced to intercept 15 one-way attack drones in a single engagement in March 2024. These naval skirmishes have necessitated persistent unmanned surveillance. Task Force 59 logged over 60,000 hours of unmanned surface vessel operations by January 2024, proving that only autonomous systems can maintain the necessary sensor mesh to protect shipping lanes without exhausting crewed ships.

Which Top Players Are Disrupting the Manufacturing Landscape?

Agile technology integrators are currently outperforming traditional defense primes in the unmanned electronic warfare market by delivering capabilities on rapid timelines. Anduril Industries stands out as a market leader, having secured a USD 249,978,466 contract in October 2024. Their commitment involves delivering over 500 Roadrunner-M units by the end of 2025. Shield AI is another dominant force, winning a USD 198 million IDIQ contract from the US Coast Guard in July 2024. Their V-BAT platform offers a crucial 10 hours of endurance for persistent surveillance.

Epirus and Fortem Technologies represent the cutting edge of engagement capabilities. Epirus demonstrated its Leonidas high-power microwave system in September 2025, achieving a 100% success rate by defeating 61 out of 61 targets. Fortem Technologies reported over 4,500 successful captures with its DroneHunter F700 system by 2025. These companies are not merely developing prototypes; they are fielding proven hardware that defines the current competitive edge of the unmanned electronic warfare market.

What Products Witness the Highest Demand?

Demand is highest for systems that combine portability with autonomous lethality. The Roadrunner-M by Anduril is a prime example of a high-demand interceptor that bridges the gap between reusable drone and loitering munition. Similarly, the Pulsar-L (Lite) system, unveiled in April 2025, weighs less than 25 lbs. Its form factor allows dismounted troops to carry advanced EW capabilities, with a deployment time of under 2 minutes.

Ground-based tactical systems also see significant procurement activity. The US Army awarded Mastodon Design (a CACI subsidiary) a USD 99.9 million contract in July 2024 for the Terrestrial Layer System-Brigade Combat Team (TLS-BCT) Manpack. Procurement documents requested 52 units for FY2024 and an additional 51 units for FY2025. These figures indicate a strong preference for modular, man-portable solutions within the broader unmanned electronic warfare market.

How Competitive Is the Market Position?

Competition is intensifying as technology firms merge with or acquire smaller specialists to expand their total addressable market (TAM). Axon Enterprise completed the acquisition of Dedrone for approximately USD 400 million in October 2024. That strategic move expanded Axon’s TAM by an estimated USD 14 billion, signaling that non-traditional defense players are entering the space.

Established defense structures are also fostering competition through initiatives like Replicator. The US DoD selected 30 unique prime contractors for Replicator awards from a pool of over 500 applicants in 2024. The Replicator 2 initiative, announced in September 2024, specifically targets C-sUAS systems with a fielding timeline of 18 to 24 months. Such accelerated procurement cycles force companies to prioritize speed of manufacturing over long-term R&D, fundamentally altering the competitive dynamics of the unmanned electronic warfare market.

What Recent Trends and Challenges Affect Market Growth?

Geopolitical posturing in the Indo-Pacific is a major trend driving capital allocation. Taiwan’s proposed special defense budget, announced in December 2025, totals NT 1.25 trillion (approx USD 40 billion). A specific allocation of NT 1.01 billion (USD 32 million) was designated in November 2025 for drone technology integration. Furthermore, the US defense bill passed in December 2025 includes USD 1 billion specifically for Taiwan security cooperation. These massive capital injections ensure sustained growth for the unmanned electronic warfare market in the Asian theater.

Rapid technological adaptation remains the primary challenge. The Silent Swarm 2024 exercise tested 57 distinct electromagnetic warfare technologies, a significant increase from 31 the previous year. However, the emergence of fiber-optic drones that are immune to jamming threatens to render radio-frequency based EW systems obsolete. Market players must now develop "cognitive" EW capabilities, as seen in the US Air Force's retrofit of 99 F-15E aircraft with the EPAWSS suite. Adapting to threats that change monthly rather than yearly is the new standard for survival in this sector.

Segmental Analysis

The Modular Payload Revolution Driving Hardware Hegemony

The dominance of Unmanned Electronic Warfare Equipment, holding a staggering 71.74% market share, is driven by a critical architectural pivot: the death of the "fixed platform" and the rise of the "modular payload." In 2024 and 2025, defense procurement shifted aggressively away from bespoke, single-mission aircraft toward the "payloadization" of effects. This segment is no longer defined by the aircraft itself, but by the interchangeable operational modules—jammers, sensors, and decoys—that adhere to the C5ISR/EW Modular Open Suite of Standards (CMOSS).

A prime driver of this hardware hegemony in the global unmanned electronic warfare market is the U.S. Army's decisive pivot in late 2025 regarding its "Launched Effects" (LE) program. By mandating the fielding of LE capabilities to every division and Multi-Domain Task Force by 2026, the market has seen an explosion in demand for miniaturized EW payloads compatible with attritable frames like the Anduril Altius 700 and Raytheon Coyote Block 3. The value lies in the volume; unlike a legacy manned jammer (like an EA-18G) which is purchased in the dozens, unmanned EW hardware is being procured in the thousands. This commoditization ensures that the equipment segment remains the financial center of gravity, as nations stockpile "spectral ammunition"—disposable jamming modules designed to be expended in the opening salvos of a peer conflict.

Survival in the Zero Trust Spectrum

The fact that Electronic Protection (EP) holds the highest capability share at 36.65% of the unmanned electronic warfare market offers the most significant tactical insight of the current era: in 2026, to emit is to die. The proliferation of "Home-on-Jam" missiles and AI-driven signal triangulation has forced unmanned systems to prioritize survival over attack.

This market segment is being propelled by the rapid integration of Cognitive Electronic Warfare (CEW). Mere pre-programmed frequency hopping is no longer sufficient against adversaries using machine learning to predict spectral maneuver. Consequently, the EP market is dominated by Cognitive AI/ML modules that allow unmanned systems to sense the electromagnetic environment and adapt their emissions in real-time, without operator input.

Furthermore, the "protection" category is expanding in the unmanned electronic warfare market to include physical hardening against non-kinetic kills. The lessons from the Ukrainian theater, where Russian EW successfully severed command links for up to 2,000 drones per week at peak intensity, have driven the standardization of Anti-Jamming Controlled Reception Pattern Antennas (CRPA) and visual navigation systems that function in GPS-denied environments. The emergence of fiber-optic guided drones—impervious to spectral interference—also falls under this logic of "protection," forcing the market to develop hybrid communication architectures that can survive the absolute denial of the RF spectrum.

The Rise of the Stand In Jammer and Ghost Fleets

The Airborne segment’s leadership (41.74% share) and high CAGR (7.82%) in the unmanned electronic warfare market is not merely about drones flying; it is about the tactical doctrine of the "Stand-in Jammer." Traditional airborne EW relied on "stand-off" platforms blasting noise from safe distances. The new doctrine requires unmanned systems to penetrate the enemy's Anti-Access/Area Denial (A2/AD) bubble and deliver jamming effects at point-blank range.

This dominance in the unmanned electronic warfare market is best exemplified by the U.S. Navy’s deployment of the NEMESIS (Netted Emulation of Multi-Element Signature against Integrated Sensors) ecosystem. By using swarms of unmanned airborne and surface vehicles to emit signals that mimic the radar cross-section of a carrier strike group, the Navy has operationalized the "Ghost Fleet" concept. The airborne segment is growing fastest because it is the primary vector for this deception. These unmanned systems do not just obscure friendly forces; they clutter enemy scopes with phantom formations, forcing adversaries to waste expensive munitions on cheap, unmanned decoys. The ability of the airborne domain to project these effects over the horizon, unlike ground or naval assets restricted by terrain and curvature, secures its market lead.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Sovereign Monopolies and the Replicator Effect

The Government & Defence category’s overwhelming 86.07% market share underscores a critical reality in the unmanned electronic warfare market: Electronic Warfare is the most jealously guarded sovereign capability. While commercial drone usage is widespread, the specific hardware required to execute high-power jamming or spectral spoofing remains strictly regulated under regimes like ITAR (International Traffic in Arms Regulations).

The projected 7.28% CAGR in this sector is heavily influenced by the U.S. Department of Defense’s "Replicator" initiative, which aimed to field thousands of autonomous systems by August 2025. This state-directed market interference has effectively nationalized the innovation pipeline. Governments are no longer waiting for the private sector to adapt commercial tech; they are issuing direct solicitations for "sovereign operational stacks." In conflict zones like Eastern Europe, the government has become the sole clearinghouse for EW technology, streamlining procurement to bypass traditional bureaucratic hurdles. Unlike the commercial surveillance drone market, where hobbyist tech plays a role, the unmanned EW market is a closed loop of state funding and state-sanctioned violence, ensuring that government contracts remain the exclusive lifeblood of the industry.

To Understand More About this Research: Request A Free Sample

Regional Analysis

The global unmanned electronic warfare market showcases varied trends and developments across different regions. Wherein, North America, Europe, and Asia-Pacific emerge as key players, each contributing uniquely to the market's growth and evolution.

Leading the charge, North America holds a commanding position with over 35.16% of the global market share. This dominance is anchored by the United States, which allocates a substantial portion of its defense budget to unmanned electronic warfare. The U.S. Department of Defense has increased its spending on these technologies by 20% annually, reflecting a strong commitment to maintaining its strategic edge. Notably, 60% of all U.S. military drones are now equipped with advanced electronic warfare capabilities. The region's market growth is further propelled by robust research and development initiatives. For instance, in 2022, the U.S. invested approximately $1.5 billion in developing next-generation electronic warfare systems, a 25% increase from the previous year. This investment underscores the region's focus on innovation and technological superiority in unmanned electronic warfare.

Europe follows North America in the unmanned electronic warfare market. The region’s market share is bolstered by collaborative defense projects among member states, notably within the framework of the European Union and NATO. European defense spending on unmanned electronic warfare has seen a steady rise of 15% over the past five years. Countries like the United Kingdom, France, and Germany are leading the way, with each nation allocating over 20% of their respective defense budgets to unmanned electronic warfare systems. In recent years, the European market has witnessed a 30% increase in the deployment of unmanned aerial vehicles (UAVs) for electronic warfare purposes, highlighting the region's strategic emphasis on these technologies.

The Asia-Pacific region, though trailing behind North America and Europe, exhibits significant growth potential in the unmanned electronic warfare market. The market here is primarily driven by increasing defense expenditures and a growing focus on indigenous military capabilities. China and India, in particular, are key contributors, with each country increasing its spending on unmanned electronic warfare by 25% annually. China’s notable advancements in UAV technology have seen a 40% increase in the deployment of unmanned electronic warfare systems in the last three years. India, on the other hand, has invested heavily in developing homegrown electronic warfare capabilities, with a 30% increase in budget allocation for these technologies.

Top 5 Recent Developments in Unmanned Electronic Warfare Market

- Thales & Autonomous Devices (Sep 9, 2025): Announced partnership at DSEI 2025 to co-develop EW-UAS, a modular drone for electronic support, detection, jamming, and naval/land defense; initial testing underway.

- L3Harris & Shield AI (Sep 22, 2025): Demonstrated AI-powered passive drone detection using WESCAM MX-Series sensors and Tracker software, detecting obscured threats at longer ranges for counter-UAS integration with VAMPIRE system.

- PteroDynamics & AeroVironment (Dec 16, 2025): Showcased integrated EW capabilities on Transwing VTOL UAS during U.S. Navy Silent Swarm 25 exercise, enhancing unmanned electronic warfare performance.

- Saab & General Atomics (Dec 18, 2025): Launched strategic cooperation for Unmanned Airborne Early Warning (UAEW) solution on MQ-9B platform, integrating Saab's AEW sensors for persistent surveillance and EW in manned-unmanned teaming.

- BAE Systems & Lockheed Martin (Sep 9, 2025): Teamed to develop 1-tonne autonomous air systems focused on electronic warfare jamming to penetrate denied environments.

Top Players in the Unmanned Electronic Warfare Market

- BAE Systems

- Elbit Systems Ltd.

- General Dynamics Corporation

- L3Harris Technologies

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- ROBIN RADAR SYSTEMS

- Thales Group

- UAV Navigation

- Other Prominent Players

Market Segmentation Overview:

By Product Type

- Unmanned Electronic Warfare Equipment

- Jammers

- Directed Energy Weapons (DEWs)

- Software Defined Radio (SDR)

- Frequency Hopping (FH) Radios

- Acoustic Sensors (Microphones)

- Optical Sensors (Cameras)

- Antennas / Antenna Arrays

- Other Equipment

- Unmanned Electronic Warfare Operational Support

By Capability

- Electronic Support (ES)

- Electronic Protection (EP)

- Electronic Attack (EA)

By Platform

- Airborne

- Ground

- Space

- Naval

By Mode of Operation

- Semi-Autonomous

- Fully Autonomous

By End User

- Government & Defence

- Commercial & Industrial

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 2,728.12 Mn |

| Expected Revenue in 2035 | US$ 5,032.44 Mn |

| Historic Data | 2020-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Mn) |

| CAGR | 7.04% |

| Segments covered | By Product Type, By Capability, By Platform, By Mode of Operation, By End User, By Region |

| Key Companies | BAE Systems, Elbit Systems Ltd., General Dynamics Corporation, L3Harris Technologies, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, ROBIN RADAR SYSTEMS, Thales Group, UAV Navigation, Other Prominent Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

The unmanned electronic warfare market is poised to climb from USD 2,728.12 million in 2025 to USD 5,032.44 million by 2035, registering a 7.04% CAGR. Growth is driven by a decisive pivot toward attritable architectures—low-cost, expendable swarm systems designed to overwhelm expensive legacy defenses.

With a 41.74% market share and the highest CAGR of 7.82%, airborne systems are critical for Stand-in Jammer tactics. Unlike ground assets, these drones penetrate A2/AD bubbles to deliver point-blank jamming, operationalizing Ghost Fleet deception concepts that saturate enemy sensors.

Asymmetric cost-exchange ratios are decisive. Data from August 2025 reveals USD 2,500 interceptor drones defeating targets valued at USD 50,000. To sustain modern wars of attrition, military planners must prioritize financially sustainable, high-volume automated defenses over exquisite manned platforms.

New fiber-optic guided drones are immune to traditional RF jamming. This forces the unmanned electronic warfare market to evolve beyond soft-kill methods, driving demand for kinetic interceptors capable of physical destruction at ranges up to 60 km to counter unjammable threats.

Holding a 71.74% share, this segment thrives on the modular payload revolution. Nations are stockpiling interchangeable sensors and jammers as disposable spectral ammunition, ensuring that component volume sales significantly outstrip the procurement of the drone frames themselves.

Integrators like Anduril and Shield AI are seizing market share by delivering software-defined hardware on rapid timelines. Initiatives like the US DoD’s Replicator reward this speed, favoring the immediate manufacturing of systems like Roadrunner-M over multi-decade R&D cycles.

The Government & Defence sector holds an overwhelming 86.07% share. Strict regulations and the weaponized nature of high-power jamming make this a sovereign monopoly, driven exclusively by state-funded force protection initiatives rather than commercial adoption.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |