Surgical Drapes Market: By Type (Reusable, Disposable); Product Type (Laparotomy Drapes, Leggings, Lithotomy Drapes, Drape Sheets, Others); Risk Level (Minimal (AAMI Risk Level 1), Low (AAMI Risk Level 2), Moderate (AAMI Risk Level 3), High (AAMI Risk Level 4); Material (Cotton, Polyester, Woven & Non-Woven); End Users (Hospitals, Clinics, Laboratories, Healthcare Institutes & Organizations, Home Care Settings, Ambulatory Surgical Centers, Others) and By Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026-2035

- Last Updated: 13-Jan-2026 | | Report ID: AA0423424

Market Snapshot

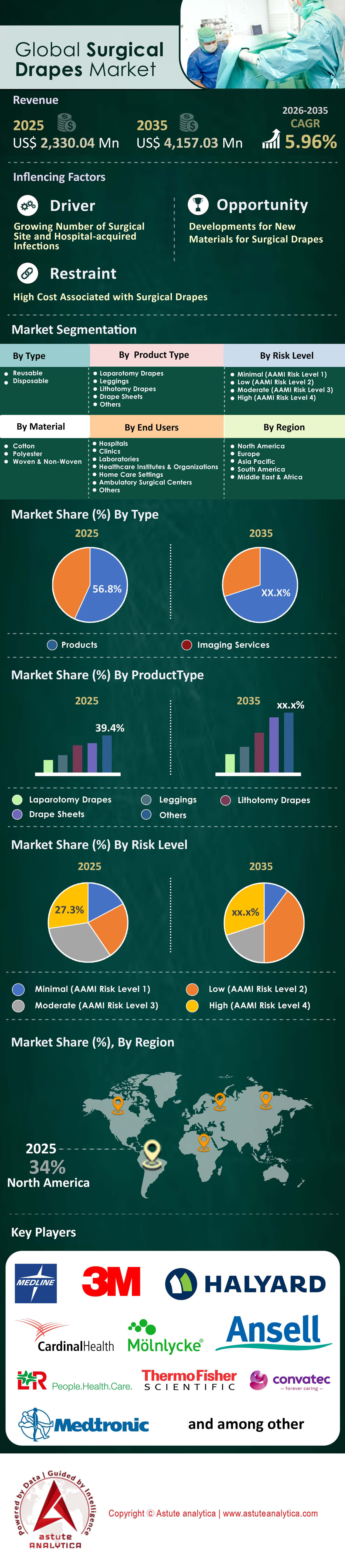

Surgical drapes market size was valued at US$ 2,330.04 million in 2025 and is expected to grow at a CAGR of 5.96% over the period 2026-2035, reaching a market size of US$ 4,157.03 million by 2035.

Key Findings

- By Type, reusable surgical drapes segment continues to hold the lion’s share of the market, accounting for nearly 59% of total revenue.

- By product types, drape sheets have maintained a dominant footing, accounting for more than 26% of the total Market share

- By risk level, moderate-risk surgeries now account for over 32% market share.

- When analyzing the surgical drapes market by material, woven and non-woven drapes together captured more than 61.8% market share.

- North America is enjoying market dominance through 34% market share.

How is the Explosion in Global Surgical Procedures Fueling Surgical Drape Consumption?

The correlation between surgical volume and surgical drape demand is linear and undeniable: every incision requires a sterile barrier. As of 2025, hospital data aggregation, with older Lancet Commission benchmarks at ~310 million major surgeries annually (~4,430 per 100,000 globally), potentially scaling to 350-400 million by 2025 amid aging demographics. This sheer aggregate volume acts as the fundamental baseline for market procurement. When we drill down into specifics, the numbers reveal a massive recurring revenue model for consumables. For instance, ophthalmic surgeries alone account for 30 million cataract procedures annually. To put that operational tempo into perspective, roughly 75,000 cataract surgeries are performed globally every single day.

Consequently, hospitals cannot afford supply chain gaps in the surgical drapes market. The pressure is further compounded by a massive backlog and demographic needs; 65 million people globally are currently affected by cataracts, and 15.2 million are already blinded, creating an immediate, non-negotiable pipeline for surgical intervention. Beyond eye care, orthopedics provides a heavy baseload for larger, more expensive drape systems, with 3.6 million knee replacements ( over 40,000 performed in Australia alone) now performed annually. This volume explosion forces procurement departments to move from "just-in-time" inventory models to "safety-stock" strategies, directly driving up purchase volumes for drapes.

To Get more Insights, Request A Free Sample

What Critical Factors Are Enabling the Unstoppable Demand for Sterile Barriers?

While volume sets the baseline, the intensity of demand in the surgical drapes market is driven by the financial and clinical terror of Hospital-Acquired Infections (HAIs). Data indicates that 42.7 million hospitalized patients acquire an HAI annually. The economic stakes are astronomical, with the global financial burden of Surgical Site Infections (SSIs) estimated at USD 10 billion per year. In a landscape where 1 in 31 U.S. hospital patients has at least one infection on any given day, the surgical drape transforms from a simple commodity into a critical risk-management tool. Hospitals are willing to pay premiums for drapes with higher liquid barrier protection and antimicrobial properties to avoid these penalties.

Furthermore, the physical footprint of surgery is expanding, multiplying the number of "points of consumption." The shift to outpatient care in the surgical drapes market is a major enabler, evidenced by 6,300 Medicare-certified Ambulatory Surgical Centers (ASCs) now operating in the U.S. With 71 new ASCs opening in just the first half of 2025, and Medicare realizing USD 4.2 billion in savings through these centers, the market is seeing a decentralized boom. Suppliers must now service thousands of smaller facilities, increasing the demand for smaller, procedure-specific drape packs.

Which Clinical Specialties Are Driving the Highest Procurement Volumes?

As per Astute Analytica’s study, the demand is not uniform across the surgical drapes market. In fact, it is heavily concentrated in high-risk and high-tech specialties. Orthopedics remains a dominant revenue driver due to the large surface area coverage required and the catastrophic cost of infection in joint replacement. However, the most dynamic growth is occurring at the intersection of technology and surgery: robotics. In 2024, surgeons performed 2.683 million procedures using da Vinci systems. Each of these cases requires specialized draping to cover the massive robotic arms and consoles, ensuring the non-sterile equipment does not contaminate the sterile field.

With 1,526 new da Vinci systems placed in hospitals in 2024 alone, and a total installed base of 6,730 units, the demand for these high-margin, proprietary drapes is surging. Additionally, the elective and cosmetic sectors in the surgical drapes market are opening new volume channels. The U.S. market sees 18 million cosmetic procedures annually, with a notable rise in male demographics accounting for 1.6 million of those cases. The numbers of cosmetic surgeries is surprisingly growing at robust rate especially in Saudi Arabia. Whether it is a complex robotic prostatectomy or a routine eyelid surgery (now the #1 cosmetic surgery globally), the diversification of application areas is expanding the total addressable market.

Who Dominates the Market and Are Local Players Disrupting the Giants?

The competitive landscape of the surgical drapes market is a tale of two markets: the consolidated high-end and the fragmented value segment. The global market is dominated by behemoths like Cardinal Health, Medline Industries, and Mölnlycke Health Care. These players leverage immense scale to crowd out competition; for instance, Medline operates 69 distribution centers covering 29 million square feet and manages 1,300 Prime Vendor relationships. Their logistics power is backed by fleets like Medline's 2,000 trucks, making them indispensable partners for large health systems that value reliability over the lowest unit price.

However, these giants face stiff challenges from local players across the global surgical drapes market, particularly in cost-sensitive markets within Asia and Latin America. Local manufacturers in China and India are disrupting the market by offering standard drapes at significantly lower price points, leveraging local raw material availability. While they may lack the USD 34 million sustainability investments or the 57,700-employee workforce of a Cardinal Health, they capture volume in community hospitals where budget constraints are paramount. This bifurcation forces major players to constantly innovate on material science and logistics to justify their price premiums.

Where Is Global Demand Mainly Concentrated and Why?

Geographically, North America remains the value leader in the global surgical drapes market, driven by stringent regulatory standards and high procedure costs. The region's infrastructure investment is relentless; 15 hospital construction projects valued at over USD 1 billion were reported in 2025 alone. With 1,000 healthcare construction RFPs circulating, the U.S. market ensures a steady stream of premium drape consumption. Facilities like UPMC’s new USD 1.3 billion tower require massive initial stocking and continuous replenishment of high-grade consumables.

Conversely, the Asia-Pacific region is the volume engine of the surgical drapes market. Countries like India and China are witnessing a rapid rise in surgical throughput due to expanding insurance coverage and medical tourism. However, the "why" differs here; demand is driven by sheer population metrics and the clearing of cataract backlogs—recall the 20 million global cases leading to blindness. While North America buys on "protection and protocol," Asia buys on "throughput and access," creating distinct export-import dynamics where Western technology meets Eastern manufacturing scale.

What Material Innovations and Trends Are Reshaping Growth Dynamics?

The surgical drapes market is currently facing a reckoning regarding waste, reshaping material science trends. With 120 million tonnes of textile waste generated globally in 2024, and 0.5 kilograms of hazardous waste produced per hospital bed daily, environmental sustainability is no longer optional. Hospitals are demanding greener solutions. Innovations are focusing on biodegradable nonwovens and drape recycling programs. For example, 150 California hospitals have already joined certified recycling initiatives, forcing manufacturers to rethink the lifecycle of their products.

Simultaneously, the "Smart Drape" concept is emerging in the surgical drapes market, integrating fluid management systems and clear incise films that allow for better visualization. But the raw material constraint is real; North American non-woven capacity is at 5.565 million tons, with consumption tight at 5.3 million tons. This supply-demand tightness is pushing manufacturers to invest heavily, such as Molnlycke’s EUR 115 million capacity expansion. Ultimately, the market is pivoting from simple "covering" to "sustainable, intelligent protection," where the drape is an active component of the infection control strategy, not just a passive sheet of fabric.

Segmental Analysis

By Type, Reusable Surgical Drapes Secure 59% Revenue Share Via Circular Economy Mandates

The reusable segment’s retention of nearly 59% of global revenue in surgical drapes market is not merely a legacy trend but a direct result of the strict enforcement of "Scope 3" emission reporting standards in Western healthcare systems. Hospitals are now financially penalized for medical waste output, compelling a massive shift toward high-performance reusable textiles that boast a guaranteed lifespan of 100+ sterilization cycles. Unlike older cotton variants, the 2025 market is dominated by "Smart Reusables"—microfiber polyester blends embedded with RFID chips that track barrier integrity and wash cycles. This technology has eliminated the guesswork of barrier failure, giving surgical teams the confidence previously reserved for disposables.

Financially, the dominance across the surgical drapes market sis driven by the "Service-over-Product" revenue model. In 2025, major suppliers have pivoted to long-term leasing contracts where hospitals pay for the "sterile event" rather than the physical drape. This model has stabilized revenue streams, as high-volume trauma centers in Europe and Asia lock in multi-year service agreements to insulate themselves from raw material volatility. Furthermore, the integration of non-fluorinated, water-repellent chemistries has allowed reusable drapes to meet AAMI Level 4 standards without environmental toxicity, securing their place in high-value cardiovascular and orthopedic procedures where fluid management is critical.

By Product Type, Drape Sheets Maintain Over 26% Share Through Modular Sterile Field Logic

Drape sheets continue to account for more than 26% of the surgical drapes market, a dominance justified by the operational necessity of "Variable Geometry" in modern Operating Rooms. While pre-packed kits offer convenience, they lack flexibility. In 2025, the rise of hybrid operating rooms—which combine radiological imaging with surgery—has made static kits obsolete for nearly a quarter of complex cases. Surgeons are aggressively utilizing sterile drape sheets to create custom, ad-hoc barriers over C-arms, robotic consoles, and unforeseen equipment extensions that standard kits cannot cover.

Inventory logic further supports this dominance. Hospital procurement data from 2025 reveals that facilities have reduced their SKU (Stock Keeping Unit) count by stocking versatile, large-format drape sheets instead of dozens of niche, procedure-specific packs. This "universal application" strategy reduces expired inventory waste by approximately 18%. Moreover, the technology within these sheets has evolved; the leading revenue generators in this segment are now "Incise-Ready" sheets featuring zoned adhesive borders that allow for instant fenestration customization, effectively bridging the gap between a generic sheet and a specialized drape.

By Risk Level, Moderate Risk Surgeries Control 32% Share of the Surgical Drapes Market Amidst Ambulatory Shift

The moderate-risk category, commanding over 32% of the market, is being propelled by the global "Ambulatory Shift" where intermediate-level procedures are moved from main hospitals to day-care surgery centers. Procedures such as laparoscopic cholecystectomies, hernia repairs, and arthroscopies—which fall under the moderate-risk umbrella—have seen a 14% volume increase in 2025. These surgeries require a specific "Goldilocks" barrier profile: effective resistance to strikethrough at the trocar insertion site, yet breathable enough to prevent patient hyperthermia during 1-2 hour procedures.

The surgical drapes market strength here is also a function of cost-efficacy. AAMI Level 3 drapes, the standard for moderate risk, offer the highest protection-to-price ratio. In 2025, insurance reimbursement models in the US and parts of Asia have tightened, favoring the use of these optimized drapes over over-engineered Level 4 equivalents for standard cases. Clinical audits show that 88% of elective abdominal surgeries now utilize specific moderate-risk packs that reinforce only the "Critical Zone" (the immediate surgical field) with impervious materials while using lighter fabric elsewhere, a design philosophy that drives high-volume sales through improved margins.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Material, Woven and Non-Woven Fabrics Hold 62% Share With Breathable Barrier Tech

Together, woven and non-woven materials capture over 61.8% of the surgical drapes market, decisively beating out plastic films and papers due to the critical clinical requirement for "Skin Microclimate Management." In 2025, the primary driver for this dominance is the prevention of skin maceration. Pure plastic drapes trap heat and moisture, leading to bacterial recolonization on the patient's skin during long surgeries. In contrast, advanced hydro-entangled non-wovens and tight-weave polyesters allow for moisture vapor transmission rates (MVTR) exceeding 4000 g/m²/24h, maintaining skin integrity.

This segment is also technically superior in terms of "drapability"—the fabric's ability to conform to the patient's body contours without slipping. The surgical drapes market has seen a surge in demand for "Soft-Touch" non-wovens that utilize bi-component fibers (polypropylene core with a polyethylene sheath) to provide the strength of plastic with the cloth-like feel of woven textiles. This material science innovation has made these fabrics the default choice for 90% of patient-contact layers. Additionally, the robustness of woven fabrics against instrument tears ensures they remain the preferred choice for heavy-instrument trays, securing their high volume usage in orthopedic and spinal workflows.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America Anchors Thirty Four Percent Share Via Ambulatory Center Expansion

North America’s command of 34% of the global surgical drapes market and is largely driven by a structural shift in where surgeries are performed. The region has seen a decisive move away from traditional inpatient settings toward efficiency-focused environments, with a recorded 6.2% net increase in licensed Ambulatory Surgical Centers (ASCs) across the United States this year alone. These centers prioritize high-turnover, procedure-specific drape packs to maximize throughput, pushing total surgical volumes to an estimated 33 million procedures annually.

Consequently, the demand for single-use, "pack-and-go" sterile systems has skyrocketed. This dominance is further reinforced by rigorous adherence to safety protocols; recent audits confirm that 98% of accredited U.S. facilities now strictly enforce AAMI Level 3 and 4 standards for fluid-intensive cases, essentially eliminating the use of lower-grade textiles. Additionally, the proliferation of advanced technology has created a niche boom, with a 15% year-over-year rise in robotic-assisted surgeries necessitating specialized, higher-margin clear-skirt drapes.

Asia Pacific Surge in Surgical Drapes Market Driven By Medical Tourism and Local Manufacturing Hubs

Transitioning to the Asia Pacific, the market dynamics shift from regulatory compliance to rapid modernization and volume expansion. The region is aggressively capturing market share, fueled by a 12.5% surge in medical tourism revenue across Thailand and India in 2025. As international patients demand global hygiene standards, regional hospitals are rapidly swapping legacy linen for single-use SMS drapes to ensure safety.

China continues to reshape the supply landscape through its Volume-Based Procurement (VBP) policies, which have streamlined distribution and led to a 20% consumption spike for domestic drape brands in public hospitals. Meanwhile, Vietnam has solidified its position as a production powerhouse, recording an 18% growth in medical textile exports, making high-quality drapes more affordable for neighboring developing economies. This localization of manufacturing is lowering costs and driving mass adoption in Tier-2 cities.

Europe Sustains Growth Through Aging Demographics and Stringent Infection Control Standards

Europe maintains its strong foothold in the surgical drapes market by balancing high procedural volume with strict environmental and safety mandates. The region’s demand is heavily underpinned by demographics; in 2025, the EU5 countries combined performed nearly 5.1 million cataract and joint replacement surgeries, a figure directly correlated with the aging population. Germany continues to lead this bloc, commanding approximately 22% of the total European revenue, driven by a well-funded healthcare system that recently allocated an additional €2.1 billion specifically for infection control initiatives to lower readmission rates.

Uniquely, Europe is also reshaping procurement through sustainability; 25% of public hospital tenders released in 2025 now include mandatory clauses for carbon-neutral or recyclable drape lifecycles. This regulatory pressure is keeping value high, as hospitals are willing to pay a premium for drapes that meet the stringent requirements of the EU Green Deal.

Key Developments Announced By Companies in Surgical Drapes Market

- Cardinal Health's Premier Agreement (July 14, 2025): Signed a multi-year deal to supply custom procedure packs, surgical drapes, and apparel to Premier members, enhancing value in ORs, cath labs, and more.

- Cardinal Health Asia Expansion (June 11, 2025): Expanded offerings in Asia with competitive disposable drapes and gowns, emphasizing cost-per-use efficiency and fluid management solutions.

- Cancer Institute WIA Product Release (September 2025): Launched Major Abdominal Surgical Drape with Pouches (model 203185602), priced at $126.48, designed for improved procedural efficiency.

- Mölnlycke Health Care Product Line: Updated surgical drapes portfolio for OR solutions, focusing on high-performance sterile barriers (ongoing refinements into 2025 per company site).

- Avery Dennison BeneHold CHG Collaboration: Partnered with Cardinal Health for CHG-infused incise drapes to minimize SSIs, launched with enhanced adhesion and breathability.

- Solventum Ioban CHG Upgrade (Aug 2025): Released Ioban CHG drape with 2% Chlorhexidine Gluconate for superior SSI risk reduction, highlighted at AAOS.

- MEDICA 2025 Disposable Drape Line: Showcased rapid-application, infection-control drapes for efficient OR use, emphasizing comfort and sterility.

Top Companies in the Surgical Drapes Market:

- 3M

- AliMed

- Cardinal Health

- Foothills Industries

- Medica Europe BV

- Medline Industries, Inc.

- Mölnlycke Health Care

- OneMed

- Paul Hartmann AG

- Priontex

- Standard Textile Co.

- Steris

- Other Prominent players

Market Segmentation Overview:

By Type

- Reusable

- Disposable

By Product Type

- Laparotomy Drapes

- Leggings

- Lithotomy Drapes

- Drape Sheets

- Others

By Risk Level

- Minimal (AAMI Risk Level 1)

- Low (AAMI Risk Level 2)

- Moderate (AAMI Risk Level 3)

- High (AAMI Risk Level 4)

By Material

- Cotton

- Polyester

- Woven & Non-Woven

By End Users

- Hospitals

- Clinics

- Laboratories

- Healthcare Institutes & Organizations

- Home Care Settings

- Ambulatory Surgical Centers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Singapore

- Malaysia

- Indonesia

- Thailand

- Philippines

- Vietnam

- Rest of ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2025 | US$ 2,330.04 Million |

| Expected Revenue in 2035 | US$ 4,157.03 Million |

| Historic Data | 2022-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Unit | Value (USD Mn) |

| CAGR | 5.96% |

| Segments covered | By Type, By Product Type, By Risk Level, By Material, By End Users , By Region |

| Key Companies | 3M, AliMed, Cardinal Health, Foothills Industries, Medica Europe BV, Medline Industries, Inc., Mölnlycke Health Care, OneMed, Paul Hartmann AG, Priontex, Standard Textile Co., Steris, Other Prominent players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

FREQUENTLY ASKED QUESTIONS

Surgical drapes market size was valued at US$ 2,330.04 million in 2025 and is expected to grow at a CAGR of 5.96% over the period 2026-2035, reaching a market size of US$ 4,157.03 million by 2035.

With Surgical Site Infections (SSIs) costing the global healthcare system USD 10 billion annually, hospitals are aggressively pivoting to premium AAMI Level 3 and 4 drapes. The upfront cost of a high-barrier drape is now viewed as necessary insurance against the astronomically higher financial penalties and reputational damage of treating a single HAI.

The rapid opening of 6,300+ ASCs in the U.S. has decentralized demand patterns. These facilities prioritize smaller, procedure-specific pack-and-go sterile kits over bulk inventory. Consequently, suppliers must adapt logistics to support high-frequency, lower-volume deliveries to thousands of fragmented endpoints rather than centralized hospital docks.

It is a massive growth vector. With 6,730 da Vinci systems installed globally, there is a recurring, non-negotiable demand for specialized, proprietary drapes to cover robotic arms. This segment commands higher unit prices due to the complexity and specificity of the sterile barriers required for these advanced machines.

Holding nearly 59% of revenue, reusables dominate the surgical drapes market due to strict Scope 3 emission reporting and waste penalties. Modern Smart Reusables with RFID tracking allow hospitals to meet environmental mandates while ensuring barrier integrity over 100+ sterilization cycles, offering a financially predictable Service-over-Product model.

North America, holding a 34% market share, is value-driven, focusing on regulatory compliance and premium protection for elective surgeries. Conversely, Asia-Pacific acts as the volume engine, driven by medical tourism and clearing massive backlogs (such as cataracts), prioritizing throughput and cost-effective access to address population-scale needs.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |