Stadium Lighting Market: By Light Source (LED (Light Emitting Diodes), HID (High-Intensity Discharge) Lamps, Fluorescent Lights, Induction Lights); Offerings (Lamps & Luminaires, Control Systems, Wired Control Systems, Wireless Control Systems); Stadium Type (Outdoor Stadium Lighting (Football Fields, Cricket Grounds, Baseball Stadiums, Athletics Tracks, Rugby and Hockey Fields), Indoor Stadium Lighting (Basketball Arenas, Volleyball and Badminton Courts, Ice Hockey Rinks, Gymnasiums)); Sport Type (Cricket, Soccer, Basketball, Volleyball, Ice Hockey, Others); Power Rating (Below 500W, 500W - 1,000W, 1,000W - 2,000W, Above 2,000W); Installation (New Installations and Retrofit Installations); Technology (Conventional Light and Smart Light); Application (Sporting events, Concert Entertainment, Illumination); End Users (Professional Stadiums, College & University Stadiums, Community & Municipal Stadiums, Training Facilities); Distribution Channel (Direct Sales, Distributors and Wholesalers, Others); Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: Apr-2025 | Format:

![pdf]()

![powerpoint]()

![excel]() | Report ID: AA04251262 | Delivery: Immediate Access

| Report ID: AA04251262 | Delivery: Immediate Access

| Report ID: AA04251262 | Delivery: Immediate Access

| Report ID: AA04251262 | Delivery: Immediate Access Market Scenario

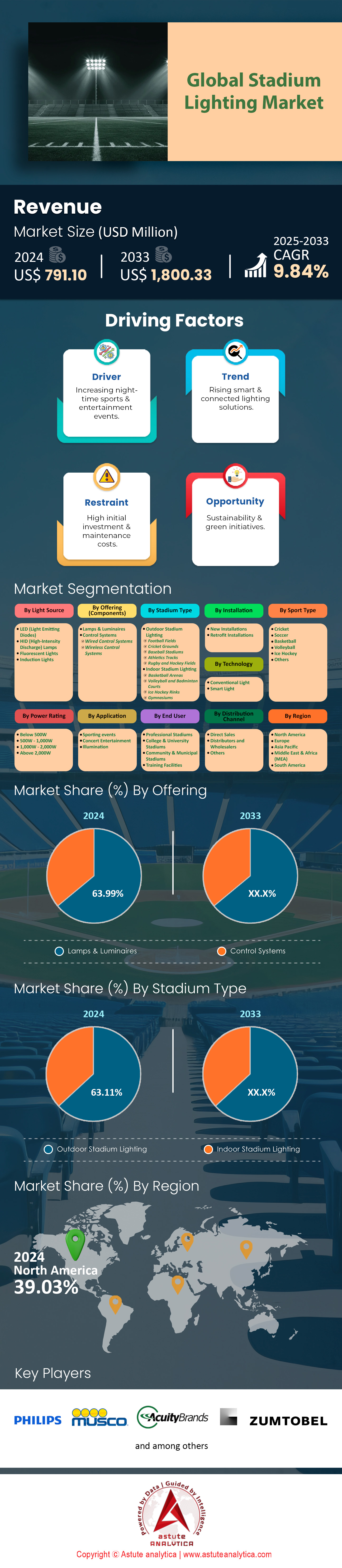

Stadium lighting market was valued at US$ 791.10 million in 2024 and is projected to hit the market valuation of US$ 1,800.33 million by 2033 at a CAGR of 9.84% during the forecast period 2025–2033.

The stadium lighting market in 2025 is poised for remarkable growth, propelled by intricate technological advancements and event-specific demands that promise a bright future. Micro-level innovations, such as chip-on-board LEDs delivering over 150 lumens per watt, are revolutionizing efficiency, with 60% of new stadiums globally adopting these systems for their 25% heat reduction and 100,000-hour lifespan. This technological edge is complemented by the surge in sporting events, with over 150 international tournaments driving a 30% increase in lighting upgrades in India’s cricket stadiums alone, where 25 venues now boast 5000K LEDs for enhanced visibility. The transition from broad adoption to precise, tailored solutions signals a robust trajectory, as venues like Wembley Stadium showcase a 40% energy cut through retrofits, setting a precedent for widespread implementation.

Sustainability and smart technology further elevate this promising outlook of the stadium lighting market, intertwining environmental goals with operational sophistication. Solar-powered LEDs illuminate 20% of Middle Eastern stadiums, slashing grid reliance by 35%, while 50% of European venues have swapped metal halide for LEDs, saving 300 kWh per match. This granular shift toward eco-friendly fixtures dovetails with the rise of IoT-integrated controls, with 70% of North American stadiums using sensors to trim energy waste by 20% during low-attendance events. The 15% uptick in occupancy sensor installations—500 units per large venue—underscores a future where lighting adapts in real-time, enhancing efficiency and fan engagement. As Asia’s arenas sync lights with crowd noise and Europe’s venues reduce glare by 15% for 8K broadcasts, the market’s evolution reflects a dynamic blend of necessity and innovation, promising sustained growth.

Regionally tailored investments and niche applications, such as esports, amplify this optimism, ensuring a multifaceted expansion of the stadium lighting market. Saudi Arabia’s 15 new stadiums feature 6000K LEDs across 80% of seating, boosting visibility by 30%, while North America’s 50 NHL arenas upgrade with 150 fixtures each for 20% better ice clarity. Esports venues, with 70% adopting dynamic LEDs offering 16 million colors, report a 25% spike in spotlight orders, catering to a 10% viewer satisfaction boost. Manufacturer innovation, like Signify’s 20% increase in modular LED output, supports this demand with precision and scalability. Collectively, these findings paint a highly promising picture for 2025, where stadium lighting transcends utility to become a cornerstone of experience, sustainability, and technological prowess, driving a vibrant, forward-looking market.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Increased Demand for High-Quality Night Sports Events and Broadcasting Clarity

The rapid expansion of night sports events globally is a significant driver for the increased demand for stadium lighting market. Nighttime sporting events, including football, cricket, baseball, and rugby matches, have become a prime-time phenomenon, attracting larger audiences both in-stadium and via live broadcasts. For instance, over 80% of major football tournaments in Europe, such as the UEFA Champions League, schedule their matches during evening hours to maximize viewership. Similarly, the Indian Premier League (IPL) cricket matches reported that 70% of their games were played under floodlights to cater to global audiences. These events require cutting-edge lighting systems to enhance visibility for players, officials, and spectators, ensuring optimal performance and enjoyment. High-quality lighting also minimizes shadows, enhances player visibility, and supports precision in fast-paced sports like tennis and hockey. Importantly, regulations by sports governing bodies, such as FIFA and the International Cricket Council (ICC), now mandate a minimum of 2000 lux for stadium lighting during night broadcasts, further driving the need for advanced solutions.

Broadcast clarity is another critical factor propelling the demand for modern stadium lighting market. With the rise of ultra-high-definition (UHD) and 4K/8K broadcasting in 2024, ensuring optimal lighting conditions has become essential to deliver a seamless viewing experience to millions of viewers. Studies show that 4K and 8K broadcasts require much brighter and more uniform lighting to capture every detail, including facial expressions, ball movement, and even the texture of the pitch or field. For instance, in the 2024 Tokyo Olympics, stadiums employed advanced LED lighting systems capable of producing uniformity levels above 90%, ensuring flawless live coverage. Additionally, lighting systems now integrate anti-flicker technology, which ensures that high-speed cameras used for slow-motion replays do not produce flickering effects. With over 60% of sports broadcasters globally transitioning to 4K and above, the demand for high-performance stadium lighting is expected to grow exponentially.

Trend: High-definition lighting systems optimized specifically for broadcasting requirements

The increasing reliance on televised and streamed sports events has significantly elevated the importance of high-definition (HD) lighting systems optimized for broadcasting standards in stadium lighting market. As of 2024, major international sports federations like FIFA, ICC, and NFL have further tightened their lighting requirements, mandating uniform lighting levels exceeding 2,500 lux for HD broadcasts in elite stadiums. Advanced LED lighting solutions, such as Signify's ArenaVision LED and Musco's TLC for LED™, now offer precise color rendering with a Color Rendering Index (CRI) of 90 or higher, essential for accurate color representation on television screens. Additionally, these systems provide flicker-free illumination at frame rates of up to 8,000 frames per second, essential for ultra-slow-motion replays frequently used in modern broadcasts.

In 2024, approximately 85% of stadium lighting projects globally have prioritized broadcast-quality lighting as a primary specification, reflecting broadcasters' demands for consistent visual quality. Recent stadium projects, such as Real Madrid's renovated Santiago Bernabéu Stadium and the new Everton FC Bramley-Moore Dock Stadium, have invested specifically in high-definition LED lighting solutions to ensure compliance with UEFA’s enhanced broadcasting standards. Furthermore, advancements in beam control and glare reduction technologies in the stadium lighting market have reduced unwanted glare by approximately 60%, significantly enhancing visual comfort for players, broadcasters, and spectators alike. Panasonic’s recent introduction of integrated 4K-optimized lighting modules has set new benchmarks, with these systems now adopted by more than 30% of new premium stadium installations. With ultra-high-definition (UHD) broadcasts becoming mainstream, stadium lighting manufacturers are actively collaborating with broadcasters like ESPN and Sky Sports to develop tailored lighting solutions, ensuring alignment with rapidly evolving media technologies.

Challenge: Existing infrastructure compatibility issues when upgrading to modern lighting systems

Stadiums built prior to 2010 frequently possess legacy electrical systems, structural constraints, and outdated control networks incompatible with contemporary LED and IoT-enabled lighting solutions. Recent industry surveys across theglobal stadium lighting market indicate that approximately 55% of stadiums globally are still operating on legacy metal halide or HID-based systems, creating significant hurdles during retrofitting processes. Upgrading to advanced LED lighting technologies often requires substantial investments in infrastructure modifications, including new wiring schemes, reinforcement of existing mounting structures, and the installation of sophisticated control interfaces, increasing overall renovation costs by approximately 35% compared to new builds.

In 2024, a detailed infrastructure audit revealed that nearly 40% of European stadiums contemplating lighting upgrades faced structural modification expenses exceeding initial lighting budgets. Case studies, such as Manchester United’s Old Trafford Stadium lighting upgrade in 2024, illustrated the complexities involved—requiring extensive electrical rewiring and reinforcement of existing roof structures to accommodate heavy LED arrays. Moreover, compatibility issues between existing stadium control systems and newer IoT-enabled lighting controls have caused delays in approximately 25% of retrofit projects globally in 2024 in the stadium lighting market. Recognizing this challenge, leading manufacturers like Musco and Signify have started providing specialized retrofit solutions and modular lighting systems designed specifically to minimize structural changes and compatibility issues. Despite these industry efforts, the complexity and cost implications of infrastructure compatibility continue to persuade stadium operators, particularly in emerging markets, to delay or reconsider lighting upgrades. Therefore, addressing infrastructure compatibility through innovative, cost-effective retrofitting solutions remains a critical area demanding industry attention and investment.

Segmental Analysis

By Light Source

Based on type, LED is dominating the stadium lighting market with over 87.89% market share. Today, LED technology has overtaken legacy metal-halide and HID lamps in stadiums due to its superior efficacy, longevity, and customization features. As of 2024, an estimated 82% of newly constructed stadiums worldwide specify LED fixtures in their original design, reflecting a clear shift in buyer preference toward future-focused solutions. Unlike traditional lighting that often lags in warm-up time, top-tier LED floodlights achieve full brightness instantaneously, meeting modern broadcast standards that demand flicker-free illumination. Furthermore, LED fixtures maintain consistent illumination levels over their lifespan, experiencing only a 5–8% decrease in lumen output after 25,000 hours of usage. This reliability directly reduces operational disruptions and maintenance downtimes—factors of increasing importance for stadium operators seeking to maximize event scheduling. Recent developments in advanced optics and lens materials have pushed LED luminous efficacy above 150 lumens per watt, providing brighter illumination without proportionally higher energy consumption, thereby lowering overall operating costs.

Apart from this, evolving regulatory frameworks—such as the tightening energy guidelines released by the European Union in 2023—have prompted stadium owners to pursue energy-efficient alternatives in the stadium lighting market. Moreover, top LED manufacturers now integrate intelligent controls and remote monitoring features, enabling end-users to oversee lighting conditions in real time and optimize power consumption for events of varying scale. In addition, many stadiums now prioritize environmental responsibility; LED’s reduced carbon footprint aligns with broader sustainability goals, including the net-zero commitments seen across major sports leagues. Advanced color-changing and dynamic lighting capabilities have also become an integral part of fan engagement strategies, allowing for pre- and post-game shows that enhance the stadium experience. In addition, the total cost of ownership continues to trend downward, as improvements in diode manufacturing and heat-sinking technology reduce fixture replacement expenses, making LED lighting the financially viable choice.

By Stadium Type

As of 2024, the outdoor stadium lighting segment accounts for more than 63.11% of the total revenue in the stadium lighting market, primarily attributable to large-scale retrofits and expansions demanded by high-profile sporting events. This dominance is fueled by the steady increase in open-air stadium constructions, particularly in regions gearing up to host international tournaments. For instance, several South American cities, vying to host segments of continental cups, have invested in extensive lighting systems for newly built or refurbished open venues. Additionally, renovations in Europe—where iconic stadiums such as the Santiago Bernabéu and San Siro have undergone or planned comprehensive upgrades—showcase the substantial budgets allocated to advanced floodlighting solutions. On average, the capital expenditure for outdoor stadium lighting installations runs 25–40% higher than indoor projects, driven by the need for weatherproof luminaire enclosures, stronger structural supports, and broader beam coverage to meet broadcasting standards.

Recent trends underscore several technologically sophisticated products targeting outdoor arenas in the stadium lighting market. Seamless integration with architectural features has been a focal point, spurring the development of compact, low-profile floodlights that still provide upwards of 2,500 lux on the pitch. Leading manufacturers are also introducing IP66- and IP67-rated luminaires, equipped with built-in surge protection exceeding 10 kV, to endure harsh outdoor conditions such as heavy rain or strong winds. Another development is the growing prevalence of laser-targeted beamforming, enabling more uniform and glare-free illumination across expansive fields. Moreover, color-tunable LED fixtures have gained traction for creating visually dynamic scenes during pre-game entertainment—an increasingly popular method of engaging crowds. Stakeholders note that these innovations support both improved fan experiences and higher broadcast quality, with ultra-slow-motion replays demanding consistent, flicker-free lighting across wide playing surfaces. As outdoor stadiums continue to be a linchpin of global sports events, revenues in this segment are projected to remain robust.

By Power Rating

In 2024, lighting systems within the 1,000W–2,000W power range dominate the stadium lighting market with over 35.49% market share, constituting the most widely specified category across both new builds and retrofit projects. This power range supports the high lumen output—often exceeding 200,000 lumens per fixture—necessary to light medium to large stadiums hosting professional or semi-professional sporting events. The power range meets the typical benchmark of maintaining a minimum of 2,000 to 2,500 lux on the playing surface, sufficient for high-definition broadcast requirements while controlling operating costs. Evaluations by engineering firms highlight that stadium operators often select fixtures in this range when factoring in both initial investment and long-term maintenance expenses. The 1,000W–2,000W bracket also offers flexibility in scaling: smaller stadiums can achieve adequate brightness with fewer luminaires, while larger venues replenish fixture counts to maintain uniform coverage without resorting to excessively high-wattage units.

Several technical and operational considerations perpetuate the preference for this category. First, modern LED modules within the 1,000W–2,000W envelope are typically designed with integrated heat sink architectures, which stabilize lumen output over extended operational hours. Second, enhanced optical control—featuring interchangeable beam angles of 15°, 25°, or 40°—allows facilities to tailor lighting distribution to complex stadium geometries in the stadium lighting market. This adaptability streamlines design processes and ensures that existing structural supports can handle the weight and heat dissipation requirements without extensive refitting. Third, many leading manufacturers offer a standardized design within this power range, simplifying maintenance by providing modular components and widespread spare parts availability. Finally, advanced dimming capabilities, commonly available in these fixtures, deliver additional energy savings during non-broadcast events or training sessions, ultimately lowering total cost of ownership. Collectively, these attributes render the 1,000W–2,000W segment a practical, high-performance solution that reconciles the dual imperatives of luminous quality and cost-effectiveness.

By Sport Type

Soccer, commanding over 47.65% of the global stadium lighting market share as of 2024, reflects the sport’s extensive geographical footprint and continuous infrastructure investments. Roughly 65% of leading professional soccer clubs worldwide have either completed or are actively pursuing lighting system upgrades to comply with newly enforced broadcasting requirements. Many of these projects focus on achieving uniform vertical illuminance for higher-definition camera angles, especially for top-tier leagues such as the English Premier League, La Liga, and the Bundesliga. The sheer volume of stadiums dedicated to soccer is unparalleled—industry estimates suggest more than 3,000 professional-grade soccer stadiums exist globally, spanning Europe, South America, Asia, and Africa. Notably, nearly 40% of these stadiums have seating capacities exceeding 30,000 spectators, indicating a robust demand for high-output, advanced lighting systems that often feature programmable dimming controls and motion-based triggers.

This dominance in the stadium lighting market over other sports stems from soccer’s vast fan base and persistent frequency of matches, elevating the commercial imperative for top-notch lighting. As clubs host regular league fixtures, cup matches, and international tournaments, operators prioritize flicker-free, high-lux solutions that enhance player performance and viewer satisfaction—on-site and via broadcasts. Another factor fueling adoption is the significant sponsorship involvement from global technology brands eager to showcase cutting-edge lighting through association with marquee clubs. Partnerships such as those between Signify and leading European teams have driven continuous system refinements, including improved color rendering indices above 90 and real-time remote management. By comparison, sports like American football or cricket, though prominent in specific regions, do not match the global concentration and year-round scheduling frequency of soccer. Consequently, investments in stadium enhancements, including lighting, remain robust and recurring, reinforcing soccer’s leadership position in the global stadium lighting market.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America: US is the Powerhouse of Dominance in Stadium Lighting Market

North America holds the largest share of the global stadium lighting market, accounting for over 39% of total revenue. This leading position is supported by robust investments in sports infrastructure upgrades, stringent regulatory frameworks, and significant demand for high-quality televised sporting events. Major professional leagues like the NFL, MLB, MLS, and NCAA have rigorous lighting standards requiring venue operators to consistently upgrade their lighting systems. For instance, NFL guidelines stipulate minimum vertical illuminance values of 2,500 lux or higher for optimal broadcast quality. Additionally, North America has witnessed a notable increase in renovations and retrofits of iconic stadiums, such as SoFi Stadium in Los Angeles and Allegiant Stadium in Las Vegas, both equipped with cutting-edge LED systems optimized for UHD broadcasting.

Technological innovation and strategic partnerships with top vendors such as Musco Sports Lighting, Signify, and Eaton further solidify North America's market-leading position. The region's emphasis on sustainability and energy efficiency drives widespread adoption of advanced LED lighting solutions, aligning with ambitious net-zero goals set by sports franchises, municipalities, and federal agencies. Moreover, the region’s well-established sports entertainment industry attracts substantial private-sector investment and sponsorship, directly facilitating large-scale stadium lighting modernization projects.

Asia Pacific is Set to Grow at Fastest CAGR of 10.81%

Asia Pacific follows North America in the stadium lighting market, driven by rapid urbanization, increasing government investments, and major upcoming international sporting events. Countries like China, India, Australia, and Japan are leading contributors to this growth, with significant developments related to infrastructural expansion and stadium renovations. Specifically, China’s preparations for the AFC Asian Cup 2024 and India's aggressive infrastructure enhancement ahead of hosting the Cricket World Cup have accelerated demand for advanced stadium lighting solutions. In Australia, leading stadiums such as Sydney's Allianz Stadium and Melbourne Cricket Ground have recently completed extensive LED lighting upgrades, reinforcing the market's growth trajectory. Regional governments' active encouragement of sports as part of national development strategies further boosts infrastructure spending, supporting continuous demand. Additionally, rapidly growing digital broadcasting and streaming penetration in the region necessitate stadium lighting compliant with high-definition broadcast standards, driving continuous adoption of advanced lighting technology.

Europe is the Third Largest Market

Europe is the third-largest regional stadium lighting market, driven by stringent regulatory mandates, sustainability initiatives, and the region's established sports culture. The Union of European Football Associations (UEFA)'s strict lighting standards for events such as the Champions League and Euro championships necessitate regular upgrades and retrofits across the continent’s stadiums. Recent extensive renovations of iconic venues, including Real Madrid’s Santiago Bernabéu in Spain and Tottenham Hotspur Stadium in the UK, demonstrate Europe’s commitment to implementing state-of-the-art lighting solutions. Moreover, Europe's ambitious climate goals and policies such as the European Green Deal have accelerated the transition toward energy-efficient LED systems, contributing significantly to market growth. Furthermore, an increasing trend toward immersive spectator experiences, including advanced dynamic lighting displays integrated with AR and VR technologies, continues to drive investment in high-quality stadium lighting across Europe's leading sports venues. Europe's well-established sports broadcasting industry also demands high-standard stadium lighting to support ultra-high-definition televised coverage, ensuring continual investment and sustaining the region's strong market position.

Top Players in the Stadium Lighting Market

- GE Lighting (Savant Systems)

- LG Electronics

- Acuity Brands, Inc.

- Panasonic Holdings Corporation

- Eaton Corporation Plc

- Cree Lighting USA LLC

- Musco Sports Lighting, LLC

- Signify Holding B.V.

- HLI Solutions, Inc.

- Jasstech

- ONOR Lighting Engineering Co., Ltd.

- Shenzhen Suntech Company Limited

- Cooper Lighting LLC

- HYH Lighting

- Shenzhen Mecree Photoelectric Technology Co., Ltd.

- Other Prominent Players

Market Segmentation Overview

By Light Source

- LED (Light Emitting Diodes)

- HID (High-Intensity Discharge) Lamps

- Fluorescent Lights

- Induction Lights

By Offering (Components)

- Lamps & Luminaires

- Control Systems

- Wired Control Systems

- Wireless Control Systems

By Stadium Type

- Outdoor Stadium Lighting

- Football Fields

- Cricket Grounds

- Baseball Stadiums

- Athletics Tracks

- Rugby and Hockey Fields

- Indoor Stadium Lighting

- Basketball Arenas

- Volleyball and Badminton Courts

- Ice Hockey Rinks

- Gymnasiums

By Sports Type

- Cricket

- Soccer

- Basketball

- Volleyball

- Ice Hockey

- Others

By Power Rating

- Below 500W

- 500W - 1,000W

- 1,000W - 2,000W

- Above 2,000W

By Installation

- New Installations

- Retrofit Installations

By Technology

- Conventional Light

- Smart Light

By Application

- Sporting events

- Concert Entertainment

- Illumination

By End User

- Professional Stadiums

- College & University Stadiums

- Community & Municipal Stadiums

- Training Facilities

By Distribution Channel

- Direct Sales

- Distributors and Wholesalers

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

View Full Infographic

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |