Semiconductor Gases Market: By Type (Bulk Gases and Electronic Special Gases (ESGs); Process (Chamber Cleaning, Oxidation, Deposition, Etching, Doping and Others); Application (Semiconductor Type, PCBs, Displays, Solar (PV), LED and Others) ; Region—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2025–2033

- Last Updated: 26-Jan-2025 | | Report ID: AA0322161

Market Scenario

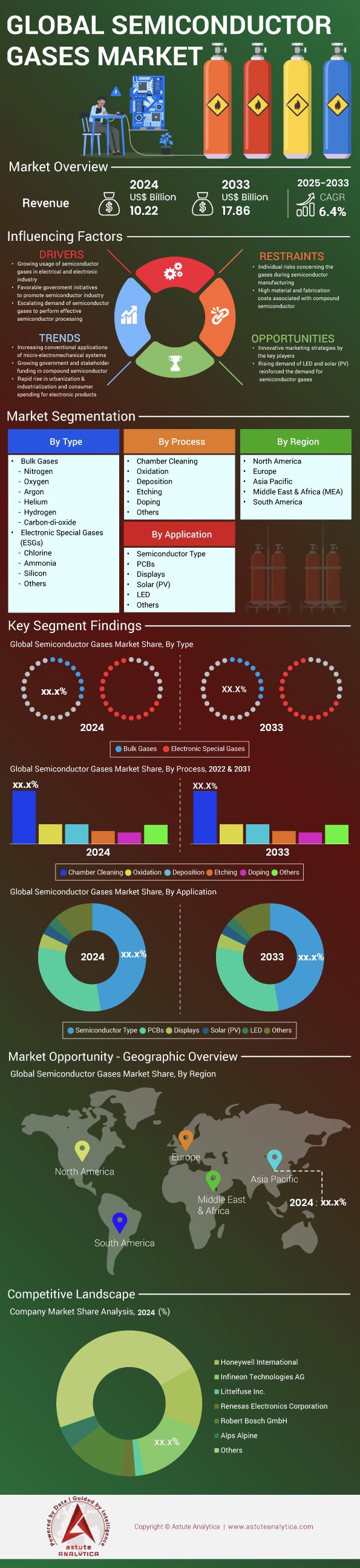

Semiconductor gases market was valued at US$ 10.22 billion in 2024 and is estimated to reach US$ 17.86 billion by 2033, at a CAGR of 6.4% during the forecast period 2025-2033.

The semiconductor gases market is surging globally, driven by the rapid expansion of advanced semiconductor manufacturing technologies. Semiconductor gases, such as nitrogen trifluoride (NF3), silane (SiH4), and hydrogen chloride (HCl), are critical in processes like etching, deposition, and cleaning. The market is reflecting the increasing adoption of high-purity gases in cutting-edge chip fabrication. Notably, nitrogen trifluoride is widely used for cleaning chemical vapor deposition chambers, while silane is essential for thin-film deposition in memory and logic chips. The United States and South Korea are leading consumers of these gases, with South Korea's semiconductor industry heavily reliant on NF3 for its advanced memory chip production. Additionally, Japan and Taiwan are key developers of high-purity gases, with companies like Air Products and Linde dominating the supply chain.

The primary driver behind the semiconductor gases market growth is the proliferation of advanced semiconductor nodes, such as 3nm and 2nm chips, which require ultra-high purity gases to ensure defect-free manufacturing. For instance, Taiwan Semiconductor Manufacturing Company (TSMC) has ramped up its use of fluorinated gases for extreme ultraviolet (EUV) lithography, a critical process for sub-5nm chips. Furthermore, the rise of electric vehicles (EVs) and 5G infrastructure has significantly increased the demand for specialty gases like hexafluoroethane (C2F6) and argon, which are used in etching and plasma processes. In 2024, the EV sector alone accounted for a substantial portion of the demand for semiconductor gases, particularly in China, where EV production is at an all-time high. Wherein, semiconductor gases are primarily deployed in fabrication facilities (fabs) for processes like etching, deposition, and cleaning. These gases are also critical for storage and transportation, requiring specialized cryogenic systems to maintain purity. Recent developments in the semiconductor gases market include the introduction of on-site bulk gas supply systems by companies like Linde, which enhance efficiency and reduce costs for fabs. The United States, Taiwan, and South Korea remain the largest consumers, while Japan and Germany are leading providers of high-purity gases. The market is poised for further growth as demand for advanced chips continues to rise globally.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Proliferation of Advanced Semiconductor Nodes Requiring Ultra-High Purity Gases

The proliferation of advanced semiconductor nodes, such as 3nm and 2nm chips, is a key driver of the semiconductor gases market. These cutting-edge chips demand ultra-high purity gases to ensure defect-free manufacturing and optimal performance. For instance, TSMC and Samsung, leaders in advanced chip production, have significantly increased their use of fluorinated gases like nitrogen trifluoride (NF3) and hexafluoroethane (C2F6) for EUV lithography and plasma etching. In 2024, TSMC alone consumed over 1,000 metric tons of NF3 for its 3nm production lines, highlighting the critical role of these gases in advanced manufacturing. Similarly, Samsung's 2nm development has driven demand for silane (SiH4) and hydrogen chloride (HCl), which are essential for thin-film deposition and cleaning processes.

The demand for these gases in the semiconductor gases market is further fueled by the growing adoption of AI and machine learning applications, which require high-performance chips. For example, NVIDIA's GPUs, widely used in AI applications, rely on advanced semiconductor nodes that necessitate ultra-high purity gases during fabrication. Additionally, the automotive sector's shift toward electric vehicles (EVs) has increased the demand for specialty gases like argon and fluorinated compounds, which are used in power semiconductor manufacturing. In 2024, the EV sector accounted for over 500 metric tons of argon consumption globally, with China leading the charge in EV production. This trend underscores the critical role of advanced semiconductor nodes in driving the demand for high-purity gases.

Trend: On-Site Bulk Gas Supply Systems Revolutionizing Semiconductor Manufacturing

A major trend in the semiconductor gases market is the adoption of on-site bulk gas supply systems, which are transforming the way fabs manage their gas requirements. Companies like Linde and Air Products have introduced innovative systems that allow semiconductor manufacturers to produce and store high-purity gases directly at their facilities. In 2024, Linde deployed over 50 on-site systems globally, with a significant concentration in Taiwan and South Korea, where leading fabs like TSMC and SK Hynix operate. These systems reduce transportation costs, minimize contamination risks, and ensure a consistent supply of critical gases like nitrogen and argon.

The trend is particularly prominent in regions with high semiconductor production, such as Taiwan, South Korea, and the United States semiconductor gases market. For instance, TSMC's new 2nm fab in Taiwan is equipped with an on-site bulk gas supply system that produces over 10,000 cubic meters of nitrogen daily. Similarly, Intel's fabs in the United States have adopted similar systems to enhance efficiency and reduce environmental impact. This shift toward on-site production is also driven by the increasing demand for sustainability in semiconductor manufacturing. By reducing the need for transportation and storage, these systems significantly lower the carbon footprint of fabs. In 2024, on-site systems accounted for over 30% of the total gas supply in leading semiconductor regions, marking a significant shift in the industry's approach to gas management.

Challenge: Ensuring Consistent Supply of Rare Gases Amid Geopolitical Tensions

One of the biggest challenges in the semiconductor gases market is ensuring a consistent supply of rare gases like neon, krypton, and xenon, which are critical for lithography and etching processes. Geopolitical tensions in the semiconductor gases market, particularly between Russia and Ukraine, have disrupted the global supply chain for these gases. Ukraine, a major supplier of neon, produced over 70% of the world's neon used in semiconductor manufacturing before the conflict. In 2024, the ongoing war significantly reduced Ukraine's neon exports, forcing semiconductor manufacturers to seek alternative sources. For instance, South Korea's SK Hynix and Samsung have turned to domestic suppliers and invested in recycling technologies to mitigate the impact of the shortage.

The challenge is further compounded by the increasing demand for rare gases in advanced semiconductor manufacturing in the semiconductor gases market. For example, ASML's EUV lithography machines, which are critical for sub-5nm chip production, require a steady supply of high-purity neon. In 2024, ASML's customers consumed over 500 metric tons of neon globally, highlighting the critical role of these gases in advanced manufacturing. To address this challenge, countries like Japan and the United States are investing in domestic production and recycling technologies. For instance, Japan's Taiyo Nippon Sanso has ramped up its production of neon and xenon to meet the growing demand. However, ensuring a consistent supply of rare gases remains a significant challenge for the semiconductor industry.

Segmental Analysis

By Type: Electronic Specialty Gases to Control Nearly 65% Market Share

Electronic specialty gases, including chlorine, ammonia, silicon compounds, and others, command the lion’s share of the semiconductor gases market, contributing around 65% of total consumption. This dominance arises from their essential roles in doping, etching, and deposition processes that form the foundation of integrated circuit manufacturing In 2024, advanced logic nodes require ultra-precise doping steps that rely heavily on ammonia-based feedstocks refined to 99.9999% purity, ensuring minimal defect rates in transistor channels Leading foundries have reported that specialized silicon precursors can enhance film deposition uniformity by up to 40% compared to older gas mixtures, driving improved device yields and performance. Next-generation packaging technologies, such as 3D stacking, have amplified the use of chlorine compounds to streamline metal etch steps, where up to 18 etch cycles can occur per device layer. The push toward even smaller geometries in logic and memory has further accelerated demand for high-purity spacial gases, underscoring the indispensability of these materials across the industry.

Key consumers in the semiconductor gases market comprise integrated device manufacturers (IDMs) and fabless companies that partner closely with semiconductor foundries, all of whom seek consistent and ultra-pure gas streams to maximize yields In 2024, at least 25 major manufacturing facilities worldwide reported advanced adoption of in-house purification systems to achieve near-trace-level contaminant detection. This shift is crucial for supporting the surge in high-performance computing, 5G networking, and AI applications, all of which demand complex chip architectures that cannot afford contamination-induced failures. As a result, producers of electronic specialty gases have expanded their R&D investments in developing specialized packaging, aligning product lines with the surging demand for advanced doping and etching. According to industry data from 2024, silicon precursor shipments grew by nearly 1.2 million liters across Asia alone, reinforcing these gases’ status as a primary driving force behind semiconductor innovation.

By Process: Chamber Cleaning to Rake in Over 30.7% of the Semiconductor Gases Market Share

Chamber cleaning is a critical operation in semiconductor fabrication, as accumulated residues must be removed from process chambers to maintain substrate purity. In 2024, advanced manufacturing lines have reported that materials like tungsten, polysilicon, and other byproducts can form deposits of up to 0.45 grams per wafer pass, requiring frequent cleaning cycles Specialized fluorinated gases and other compounds, notably nitrogen trifluoride (NF₃), have emerged as leading solutions due to their high cleaning efficiency and manageable environmental profiles Top-tier foundries typically conduct over 600 cleaning runs per month on a single 300 mm tool cluster—a figure that underscores the immense scope of gas consumption for chamber maintenance. By removing stubborn chamber deposits, these gases also extend equipment lifetime, lowering downtime costs for etch and deposition tools. The capability to clean at lower temperatures, often below 250°C, differentiates these gases from alternative methods such as plasma-based dry cleans, which can demand higher energy inputs and longer operational cycles.

In 2024, it was recorded that select fabs in the semiconductor gases market allocate up to 25% of their total process gases specifically for routine chamber conditioning, helping to ensure a defect-free environment, ensuring stable device performance. Aligned with this, new cleaning chemistries introduced in 2023 demonstrated a 12% reduction in residue accumulation, boosting overall production throughput while maintaining sub-part-per-trillion contaminant levels. Additionally, ongoing research indicates that some specialized cleaning gases can cut overall chamber cleaning time by around 27 seconds per cycle, saving manufacturers tens of thousands of dollars annually in electricity costs. These operational efficiencies are paramount in cutting-edge nodes producing 7 nm and smaller geometries, where leftover contamination can degrade transistor performance significantly. With global chipmakers requiring cleaner environments to keep pace with Moore’s Law, chamber cleaning gases have proven indispensable, establishing themselves as the preferred solution over more labor-intensive or less efficient alternatives.

By Application: Semiconductor Components Capture Over 47.4% of the Market

Semiconductor component manufacturing depends heavily on specialized gases for doping, passivation, oxidation, and related processes to build intricate device structures. Memory fabs producing DRAM and NAND chips have reported expansions to nearly 150 manufacturing steps involving gas-based operations, reflecting a surge in complexity as layer counts climb in 3D architectures. Devices in the semiconductor gases market often employ doping profiles requiring distribution of ions, such as boron or phosphorus, facilitated by high-purity phosphine or boron trifluoride feedstocks. These feedstocks must meet purity standards quantified below 10 parts per billion to guard against unwanted doping anomalies that could compromise device performance. Additionally, the advent of compound semiconductors—seen in gallium nitride (GaN) and silicon carbide (SiC)—has increased the reliance on specialty gases like trimethylgallium to achieve specific electrical and thermal characteristics tailored for power electronics. In fact, top-tier power chip makers have documented at least 22 new doping gas variants tested over the first half of 2024, underscoring the ongoing quest for optimized device reliability and efficiency.

Prominent gases in the semiconductor gases market across this application include silane for epitaxial growth, dichlorosilane for advanced deposition, and ammonia for nitride-based layers supporting everything from radio-frequency (RF) devices to micro-LED displays. Leading facilities now run as many as 80 epitaxy cycles, each requiring precision gas flows at partial pressures accurately maintained within ±0.2% tolerances. Furthermore, new doping methodologies introduced in 2023 allow high-aspect-ratio transistor gates, where specialized gases reduce the chance of sidewall voids by up to 60%. This improvement is vital as more delicate channel structures appear in next-generation mobile and server processors. The impetus behind these innovations stems from the unceasing need for higher performance, lower power consumption, and smaller form factors. Consequently, manufacturers are investing in advanced gas mixing systems, multi-layer safety protocols, and real-time purity monitoring, ensuring that every doping step meets stringent reliability targets for semiconductor components.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

Asia Pacific to Capture Over 78% Market Share of Semiconductor Gases Market

Asia Pacific dominates the global semiconductor gas consumption landscape due to a network of foundries, integrated device manufacturers, and facilities across Taiwan, South Korea, China, and Japan. As of 2024, these countries collectively operate more than 85 front-end fabrication plants that rely on volumes of gases for etch, deposition, operations The region’s robust supply chain is further amplified by dedicated local suppliers who can deliver specialized gases on short notice. According to industry surveys, advanced logic foundries in Taiwan alone have scaled to nearly 15 million wafer starts per quarter, driving significant demand for fluorides and silicon precursors. South Korean memory manufacturers have expanded their footprints with at least five new 3D NAND production lines since 2023, each requiring continuous flows of nitrogen trifluoride, silane, and ammonia to achieve multi-layer stacking and precise doping. Parallel to this, Chinese semiconductor enterprises continue to ramp up 300 mm fab projects, reportedly adding over 6 new plants in just 18 months. Such strategic expansions underscore the region’s unparalleled appetite for specialized semiconductor gases, solidifying Asia Pacific as the epicenter of leading-edge chip production.

- Thanks to Concentration of Semiconductor Manufacturing Firms

Impetus behind Asia Pacific’s leadership in the semiconductor gases market is the concentration of key industry players that have embraced integrated models. Firms like TSMC, Samsung, and SK Hynix oversee not only wafer processes but also R&D initiatives aimed at refining gas usage to shrink feature sizes and enhance yield. In 2024, a consortium of Japanese manufacturers reported breakthroughs in localized gas purification technology for extreme ultraviolet (EUV) lithography processes. This innovation, already licensed by at four other regional firms, signifies Asia’s capability to push the envelope of manufacturing precision. Meanwhile, the region invests heavily in talent development, with more than 30 specialized universities offering advanced semiconductor curricula that incorporate gas-handling safety and process simulation. The synergy of academic research, government incentives, and diverse, thriving, robust private-public partnerships ensures a steady flow of new solutions addressing the complexities of sub-5 nm node production. Taken together, these factors explain why over three-quarters of global semiconductor gases flow through Asia Pacific’s factories, fueling state-of-the-art chips for every major electronics segment from mobile devices to high-performance computing.

Top Companies in the Semiconductor Gases Market:

- Air Liquide S.A.

- Air Products Inc

- American Gas Products (AGP)

- Linde Group

- Gruppo SIAD

- Indiana Oxygen Inc.

- Iwatani Corporation

- Sumitomo Seika Chemicals Company, Ltd.

- Messer Group

- Mitsui Chemicals, Inc.

- REC Silicon ASA

- Solvay SA

- Other Players

Market Segmentation Overview:

By Type:

- Bulk Gases

- Nitrogen

- Oxygen

- Argon

- Helium

- Hydrogen

- Carbon-di-oxide

- Electronic Special Gases (ESGs)

- Chlorine

- Ammonia

- Silicon

- Others

By Process:

- Chamber Cleaning

- Oxidation

- Deposition

- Etching

- Doping

- Others

By Application:

- Semiconductor Type

- PCBs

- Displays

- Solar (PV)

- LED

- Others

By Region:

- North America

- The U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of Latin America

REPORT SCOPE

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | US$ 10.22 Bn |

| Expected Revenue in 2033 | US$ 17.86 Bn |

| Historic Data | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2033 |

| Unit | Value (USD Bn) |

| CAGR | 6.4% |

| Segments covered | By Type, By Process, By Application, By Region |

| Key Companies | Air Liquide S.A., Air Products Inc, American Gas Products (AGP), Linde Group, Gruppo SIAD, Indiana Oxygen Inc., Iwatani Corporation, Sumitomo Seika Chemicals Company, Ltd., Messer Group, Mitsui Chemicals, Inc., REC Silicon ASA, Solvay SA, Other Players |

| Customization Scope | Get your customized report as per your preference. Ask for customization |

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |