Japan Epoxy Resins Market: By Type (DGBEA (Bisphenol A and ECH), DGBEF (Bisphenol F and ECH), Novolac (Formaldehyde and Phenols), and Others); Form (Liquid, Solid, and Solution); Application (Paints & Coatings, Composites, Adhesives & Sealants, and Others); End Users (Building & Construction, Aerospace, Consumer Goods, and Others)—Industry Dynamics, Market Size and Opportunity Forecast for 2024–2032

- Last Updated: Nov-2024 | Format:

![pdf]()

![powerpoint]()

![excel]() | Report ID: AA0422199 | Delivery: 2 to 4 Hours

| Report ID: AA0422199 | Delivery: 2 to 4 Hours

| Report ID: AA0422199 | Delivery: 2 to 4 Hours

| Report ID: AA0422199 | Delivery: 2 to 4 Hours Market Scenario

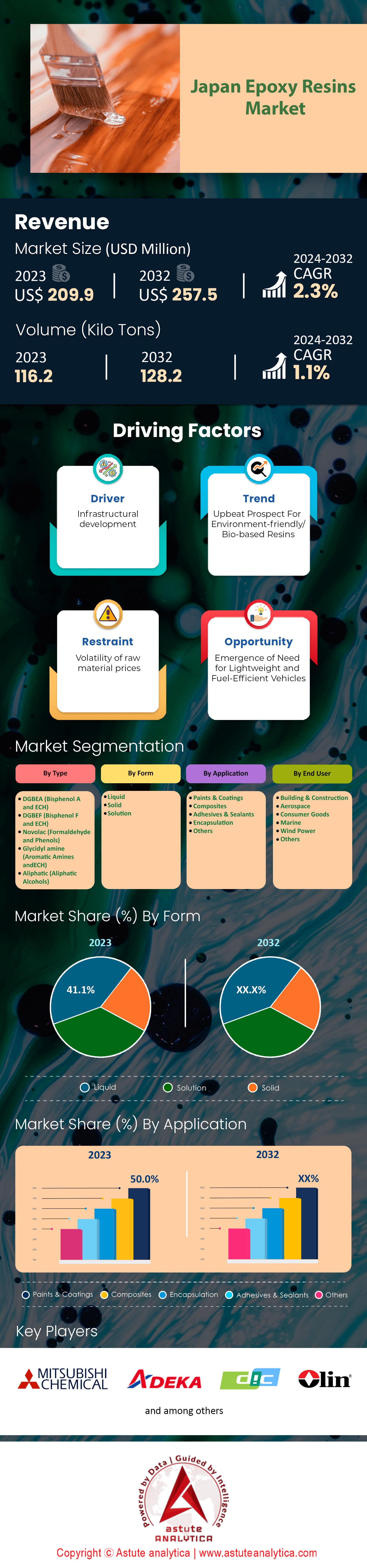

Japan epoxy resins market was valued at US$ 209.9 million in 2023 and is projected to hit the market valuation of US$ 257.5 million by 2032 at a CAGR of 2.3% during the forecast period 2024–2032.

Japan's epoxy resins market remains highly mature due to saturation in key application sectors such as automotive, electronics, and construction. Annually, Japan produces around 1.11 million tons of epoxy resin, catering to both domestic consumption and international exports. The automotive industry is one of the primary consumers; Japan manufactured about 7.8 million vehicles in 2023, utilizing epoxy resins extensively for lightweight and durable components that enhance fuel efficiency and vehicle performance. In the electronics sector, Japan continues to lead with the production of over 300 million electronic devices annually, where epoxy resins play a critical role in insulation, circuit boards, and protective encapsulation.

The construction industry significantly impacts epoxy resin demand, with approximately 850,000 new housing starts recorded in 2023. Epoxy resins are favored in construction for their strong adhesive properties and resistance to environmental degradation, essential for infrastructure longevity. Environmental concerns and stringent regulations have prompted a shift towards sustainable materials. As of 2023, Japan has initiated over 50 projects focused on developing bio-based epoxy resins, aiming to reduce reliance on petrochemical sources and lower environmental impact. The electric vehicle (EV) sector is another influential factor; Japan produced around 493,535 EVs in 2023, driving demand for specialized epoxy resins used in battery systems and electronic components essential for EV performance and safety.

Looking ahead, Japan's commitment to achieving carbon neutrality by 2050 is set to transform the epoxy resins market. The renewable energy sector is expanding rapidly, with over 1,500 megawatts of new wind and solar capacity added in 2023. These projects utilize epoxy resins in wind turbine blades and photovoltaic panels, leveraging their durability and resistance to harsh environments. Japanese companies are investing significantly in research and development, with an estimated US$ 60 million allocated in 2023 to advance high-performance epoxy resins, particularly those that are sustainable and meet environmental regulations. Strategic collaborations are increasing, with over 40 partnerships established with international firms to enhance technological capabilities and expand global market reach. The aerospace industry also presents growth opportunities; Japan plans to launch new satellite and aircraft projects requiring advanced epoxy composites known for their strength-to-weight ratio and thermal stability. Despite the slow overall growth, these developments indicate a strategic shift towards specialized applications and sustainable practices, positioning Japan's epoxy resins market for gradual yet meaningful advancement in the coming years.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Advanced Electronics Demand High-Performance Epoxy Resins for Miniaturized Circuit Boards

Japan remains a global leader in electronics manufacturing, with the country producing over 2 billion semiconductor units annually and more than 15.72 billion units of ICs were produced in Japan in 2023. The demand for advanced electronics, particularly miniaturized circuit boards, is a significant driver of epoxy resins market. These resins provide essential benefits such as electrical insulation, mechanical strength, and resistance to environmental factors, making them indispensable in high-performance electronic applications. In recent years, the miniaturization trend has accelerated, with Japanese companies like Sony and Panasonic leading the charge in developing smaller, more efficient devices. As a result, the need for epoxy resins that can withstand the rigors of miniaturization continues to grow.

The epoxy resins market in Japan's electronics sector is valued at approximately US$ 23 billion, with a projected increase as the demand for consumer electronics rises. Over 1,000 Japanese companies are involved in the production and application of epoxy resins, underlining the material's centrality to the industry. The development of 5G technology, which requires compact and efficient circuit boards, further fuels the demand for high-performance epoxy resins. Furthermore, Japanese firms are investing heavily in research and development, with over 500 million USD allocated annually to improve epoxy resin formulations for electronic applications.

Japan's focus on innovation and quality has resulted in the production of epoxy resins that meet stringent international standards. The country exports over 500,000 tons of electronic components annually, many of which incorporate advanced epoxy resins. The trend toward miniaturization is expected to continue, driven by consumer demand for portable and multifunctional devices. As such, the epoxy resins market in Japan is poised for sustained growth, supported by the electronics industry's continued evolution and the country's commitment to maintaining its position as a leader in technology and innovation.

Trend: Increased Use of Epoxy Resins in 3D Printing for Complex Structures

The adoption of 3D printing technologies across various industries in Japan epoxy resins market has seen a remarkable surge, with over 10,000 businesses currently utilizing these technologies. Among the materials used, epoxy resins have gained prominence due to their exceptional properties, such as high strength, chemical resistance, and versatility. The Japanese market for 3D printing materials, including epoxy resins, is valued at approximately US$ 1.2 billion and is expected to grow as industries recognize the potential of 3D printing for complex structures.

Epoxy resins are particularly favored in the automotive and aerospace sectors, where complex geometries and lightweight materials are paramount. Japan's automotive industry, producing over 9 million vehicles annually, increasingly incorporates 3D-printed components made from epoxy resins to enhance performance and reduce weight. Similarly, the aerospace sector in the epoxy resins market, valued at around US$ 40 billion, utilizes these resins for manufacturing lightweight and durable parts, contributing to the industry's growth. The precision and customization offered by 3D printing, combined with the strength of epoxy resins, allow for innovative designs that were previously unattainable.

Research and development in Japan play a crucial role in advancing 3D printing technologies and materials. Over US$ 200 million is invested annually in developing new resin formulations that improve printability and performance. Japanese universities and research institutions collaborate with industry leaders to push the boundaries of what is possible with 3D printing and epoxy resins. As a result, Japan is poised to remain at the forefront of 3D printing innovations, with epoxy resins playing a critical role in enabling the creation of complex, high-performance structures across various industries.

Challenge: Competition from Alternative Materials Offering Similar Performance Benefits

The Japanese epoxy resins market faces significant challenges from alternative materials that offer similar performance advantages, such as polyurethane and silicone resins. These materials are gaining traction due to their unique properties like flexibility, thermal stability, and cost-effectiveness. Japan's chemical industry, valued at over US$ 200 billion, is highly competitive, with over 2,000 companies vying for market share. This competition has intensified as alternative materials continue to evolve, providing viable options for applications traditionally dominated by epoxy resins.

One of the most significant challenges for epoxy resins market growth is the development of bio-based alternatives, which align with Japan's commitment to sustainability and environmental responsibility. The Japanese government supports initiatives to reduce carbon emissions, and the chemical industry is no exception, with over 100 projects focused on developing eco-friendly materials. This push for sustainability has led to an increased interest in bio-based resins, which offer reduced environmental impact without sacrificing performance. As a result, epoxy resins must compete with these emerging materials that cater to environmentally conscious consumers and industries.

The automotive and electronics sectors, which account for a substantial portion of epoxy resin consumption in Japan, are exploring alternative materials to meet regulatory and consumer demands for sustainability. Reports indicate that over 3,000 new products incorporating alternative resins have been developed in the past year alone. This shift presents a considerable challenge for the epoxy resins market, requiring manufacturers to innovate and differentiate their products to maintain relevance. As competition from alternative materials continues to grow, the Japanese epoxy resin industry must adapt to remain a key player in the global market.

Segmental Analysis

By Type

DGBEA also known as Bisphenol A (BPA) and Epichlorohydrin (ECH) dominate Japan's epoxy resins market with over 69.7% market share due to their exceptional properties, including high mechanical strength and thermal stability, essential for advanced industrial applications. The global production of BPA and ECH stands at approximately 7 million and 2 million metric tons, respectively, with Japan as a key contributor. In 2023, Japan's automotive industry, producing over 9 million vehicles annually, heavily relied on these resins for enhancing vehicle performance and durability. The electronics sector, valued at over $140 billion, utilizes BPA and ECH-based resins for printed circuit boards and component encapsulation, benefiting from their insulating properties. Furthermore, Japan's construction industry, with expenditures exceeding $500 billion annually, demands these resins for infrastructure projects, protective coatings, and adhesives.

Key players like Mitsubishi Chemical Corporation produce around 400,000 metric tons of BPA annually, while Sumitomo Chemical Co. outputs over 100,000 metric tons of ECH, meeting domestic and international demands. The global epoxy resins market is projected to surpass $10 billion, with Japan's significant role highlighted by its investment in renewable energy exceeding $16 billion, increasing resin use in wind turbines and solar panels. Additionally, Japan's R&D spending of over $130 billion annually encourages innovation in resin formulations. Leading consumers, including Toyota, Honda, Sony, and Panasonic, rely on these resins for high-quality, durable products. As Japan continues to emphasize technological advancement, BPA and ECH resins remain crucial, with their integration into emerging applications further solidifying their market dominance and contributing to the rising demand observed in 2023.

By Form

Liquid epoxy resins are leading the Japanese epoxy resins market due to their versatility and extensive application across key industries. In 2023, the liquid epoxy resins accounting for a substantial share of 41.1% and is poised to grow at a CAGR of 1.3% in the years to come. One of the primary drivers is the automotive industry; Japan produced around 8 million vehicles in 2023, making it one of the world's top automobile manufacturers. Liquid epoxy resins are crucial in producing lightweight composite materials used in vehicle bodies and parts, enhancing fuel efficiency and reducing emissions. The electronics sector, a significant contributor to Japan's economy with an output value exceeding 10.7 trillion yen, heavily relies on liquid epoxy resins for manufacturing printed circuit boards and semiconductor encapsulants. Additionally, the construction industry, with over 900,000 new housing starts in 2023, utilizes these resins in coatings and adhesives to improve building durability and longevity.

The demand for liquid epoxy resins market is on the rise due to their superior mechanical properties and adaptability to advanced technologies. They offer excellent adhesion, chemical resistance, and thermal stability, making them ideal for high-performance applications. Environmental concerns and stringent regulations have propelled industries to adopt materials that contribute to sustainability goals. Liquid epoxy resins enable the production of lightweight components, leading to significant reductions in carbon emissions—estimated at 5 million tons annually in Japan's transportation sector. The renewable energy industry also bolsters demand; Japan's installed wind power capacity reached 5 gigawatts in 2023, with liquid epoxy resins being essential in manufacturing wind turbine blades. Furthermore, considerable investments in research and development, totaling over US$ 2 billion in the chemical sector, have led to advanced formulations and expanded applications of liquid epoxy resins. These factors collectively reinforce the higher preference and dominance of liquid epoxy resins in the Japanese market.

By Applications

The epoxy resins market in Japan is predominantly driven by the paints and coatings application due to the extensive industrial activities and the superior properties of epoxy resins. In recent years, the consumption of epoxy resins in Japan's paints and coatings industry has been substantial and accounted for more than 50% market share. For instance, the automotive sector, a major contributor to Japan's economy with an annual production of over 9 million vehicles, significantly increases the demand for epoxy-based coatings essential for corrosion resistance and durability. The shipbuilding industry also plays a crucial role; Japan is among the top shipbuilding nations globally, producing vessels totaling millions of gross tons annually, all of which require high-performance epoxy coatings to withstand harsh marine environments.

In the construction industry, Japan has been actively involved in infrastructure projects, including the building and renovation of bridges, tunnels, and buildings. With over 800,000 new housing units constructed annually, epoxy resins are widely used in flooring and protective coatings due to their strength and resistance to wear and tear. Additionally, the electronics industry, a key sector in Japan epoxy resins market with the production of hundreds of millions of electronic devices each year, uses epoxy resins for insulating and protecting components. The demand for environmentally friendly coatings has led to increased use of waterborne epoxy resins, aligning with global sustainability efforts.

Several factors are enabling the growth of epoxy resins in Japan's paints and coatings market. The government's investment in infrastructure, including a multi-trillion yen allocation for development and maintenance projects, is driving the demand for durable coatings. The protective coatings market sees substantial activity, with thousands of industrial facilities undergoing maintenance annually, relying on epoxy resins for equipment and infrastructure protection. The automotive industry's shift towards electric vehicles, with sales numbers increasing yearly, is boosting the need for epoxy resins in battery systems and lightweight components.

By End Users

As of 2023, Japan's construction industry continues to be a cornerstone of its economy and capturing over 29.7% revenue share of the epoxy resins market. The dominance is mainly driven by rapid urban redevelopment, infrastructure renewal, and earthquake-resistant building initiatives. The industry is currently valued at approximately ¥56 trillion, with Tokyo alone accounting for ¥15 trillion due to its ongoing urban projects. This robust activity directly fuels the demand for epoxy resins, a crucial component in construction due to their adhesive, chemical-resistant, and durable properties. Recently, the Japanese government announced plans to invest ¥6 trillion in infrastructure over the next decade, focusing on enhancing the resilience of the nation's transportation and building frameworks. Additionally, there are about 2,000 ongoing high-rise projects across the country, each relying heavily on advanced materials like epoxy resins for structural integrity and longevity.

Epoxy resins find extensive applications in the construction sector, particularly in flooring, coatings, and structural adhesives. The epoxy resins market is seeing increased usage in the production of composites for bridge construction, with over 300 bridges currently being built or renovated using epoxy-based materials for their superior strength and weather resistance. Furthermore, with Japan facing over 1,500 seismic activities annually, the demand for earthquake-proofing materials has surged, positioning epoxy resins as a preferred choice for reinforcing building frameworks. This growth is also spurred by technological advancements in resin formulations, which enhance performance and sustainability. A notable trend is the adoption of eco-friendly epoxy solutions, with nearly 500 companies now offering green-certified products. This shift not only aligns with global environmental standards but also addresses local regulations aimed at reducing carbon footprints. The combination of strong government support, technological innovation, and the country's socio-economic dynamics make epoxy resins indispensable to Japan's thriving construction industry.

To Understand More About this Research: Request A Free Sample

Top Players in Japan Epoxy Resins Market

- The 3M Company

- Aditya Birla Chemicals

- Arkema

- BASF SE

- Covestro AG

- Cytec Solvay Industries

- DuPont

- Evonik Industries

- Huntsman International LLC

- Jiangsu Sanmu Group

- Jubail Chemical Industries

- Kukdo Chemical Co. Ltd.

- MPM Holdings

- Olin Corporation

- Sinopec Corporation

- Sika AG

- Hitachi Automotive Sys

- Toray International Inc.

- Dic Corporation

- Kaneka Corporation

- Other Prominent Players

Market Segmentation Overview:

By Type:

- DGBEA (Bisphenol A and ECH)

- DGBEF (Bisphenol F and ECH)

- Novolac (Formaldehyde and Phenols)

- Glycidyl amine (Aromatic Amines and ECH)

- Aliphatic (Aliphatic Alcohols)

- Others

By Form:

- Liquid

- Solid

- Solution

By Application:

- Paints & Coatings

- Composites

- Adhesives & Sealants

- Encapsulation

- Others

By End User:

- Building & Construction

- Aerospace

- Consumer Goods

- Marine

- Wind Power

- Others

View Full Infographic

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Choose License Type

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |