Global D-dimer Testing Market: By Testing Method (Laboratory and Point-Of-Care); Application (Deep vein Thrombosis (DVT), Disseminated intravascular Coagulation, Pulmonary Embolism (PE), Stroke); End User (Hospitals & Clinics, Diagnostic Centers, Research Institutions, and Others); Country—Market Size, Industry Dynamics, Opportunity Analysis and Forecast For 2024–2032

- Last Updated: 23-Apr-2024 | | Report ID: AA0424820

Market Scenario

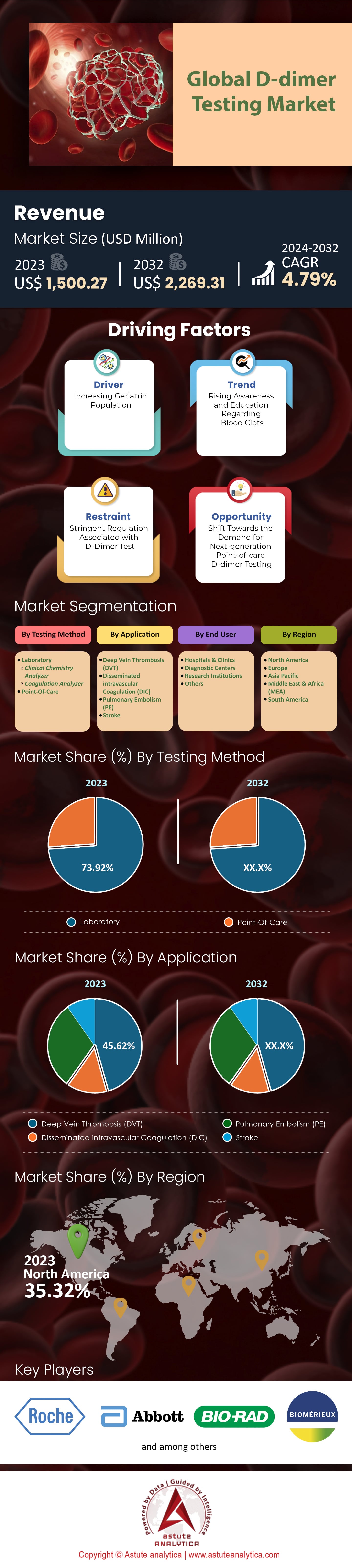

The Global D-dimer testing market was valued at US$ 1,500.27 million in 2023 and is projected to hit the market valuation of US$ 2,269.31 million by 2032, at a CAGR of 4.79% during the forecast period 2024–2032.

The D-dimer test is being demanded all over the world, for some reasons. First, there is a huge increase in the number of venous thromboembolism (VTE) cases and clotting disorders globally. For example, VTE causes about 75,000 deaths annually in America only. This growing burden of VTE calls for reliable cost-effective diagnostic tools like D-dimer testing. Furthermore, cost effectiveness and high accuracy are among the qualities that have made healthcare providers to choose D-dimers tests. It provides a non-invasive inexpensive way of ruling out blood clots thus reducing expensive invasive diagnostic methods. Besides having a negative predictive value of up-to 99% which excludes VTE other than that its sensitivity is also very high.

Also, increased occurrences of cardiovascular diseases that lead to dangerous clots in lungs contribute significantly towards this demand for D-dimer testing market. Cardiovascular diseases worldwide are leading cause of deaths each year. The global number of hospital admissions due to pulmonary embolism is also rising hence fostering its adoption worldwide. Real-time monitoring through diagnosing disseminated intravascular coagulation (DIC) early using d dimers allows interventions at once thereby improving outcomes among patients.

D-dimer testing market expansion comes as next generation point-of-care (POC) solutions are being developed which facilitate quicker diagnoses lower down waiting times improve patient satisfaction rates. These new POC devices such as AQT90 FLEX analyzer enable accessibilities convenience with regards where when performed by whom etcetera should be done so on. Another tendency involves integrating multi-marker panels used for detecting sepsis or cardiac ailments together with DDTM testing kits; this offers wider scope assessment while informing stratifications personalized based on patient’s diagnosis treatment plan besides prognosis management.

To Get more Insights, Request A Free Sample

Market Dynamics

Driver: Rising Prevalence of Venous Thromboembolism (VTE) and Blood Clotting Disorders Driving High Demand for D-dimer Testing

The public health importance of venous thromboembolism (VTE), which encompasses deep vein thrombosis (DVT) and pulmonary embolism (PE), cannot be overemphasized. In the United States alone, VTE kills about 75,000 people annually as per the CDC. Its occurrence is estimated at 1 to 2 cases per year for every 1,000 persons whereby the number rises sharply after age 45. In this country up to one million individuals may be affected by VTE each year and between 10% and 30% will die within the first month after being diagnosed with it. Worldwide, there are more than ten million cases of venous thromboembolic disease recorded every year.

Another reason why D-dimer tests are needed is because blood clotting disorders in the D-dimer testing market. Genetic variations that affect blood coagulation occur in approximately one out of 500 to a 1,000 people within the general population while 5% – 8% have one or more genetic risk factors for VTE in America alone; some types such as DIC can result into death rates exceeding 50% if left untreated. These examinations play a significant role in diagnosing or ruling out DVTs but they are also used when monitoring responses to treatments among patients who suffer from various abnormal states associated with coagulopathies. Therefore, considering global surge rates in these lethal illnesses worldwide during coming years will greatly heighten demands for D dimer testing around earth however positive results only indicate presence any clotting disorder thus mandating additional tests prior confirmation.

Trend: Growing Emphasis on High Sensitivity Assay

Compared to point-of-care tests, high-sensitivity D-dimer assays are now widely used for diagnosing venous thromboembolism (VTE) in the global D-dimer testing market because of their enhanced accuracy. Conversely, a point-of-care test has 85% sensitivity while high-sensitivity D-dimer assay has 95%. However, specificity ranges from 40% to 70% for high-sensitivity assays and from 25% to 65% for point-of-care tests. These have been found very sensitive in detecting pulmonary embolism (PE) where they had a sensitivity of 95% and specificity of 45% in an evaluation involving 808 patients with this condition. Moreover, heparin therapy was withheld at all our institutions on weekends for patients who had negative low-yield high-sensitivity D-dimer tests; no cases of deep vein thrombosis were missed during this time period.

By using age-adjusted cut-offs along with highly sensitive d-dimer tests it’s possible to obtain a specificity level as high as between 70-75 % among those aged over 50 years thereby reducing false positive results. A number of studies were brought together into one meta-analysis, which showed that they had a combined sensitivity rate equalling around 97% but only 42% specificities towards venous thromboembolism detection. Unlike point-of-care methods the higher detection limit for hs-d dimers is considered good enough since it can go down up to one tenth μg/mL compared against half micrograms per millilitre used by other approaches. Therefore, many guidelines in the global D-dimer testing market recommend its use as best rule out test among low-risk individuals.

When different types were compared during a clinical trial designed specifically around finding out what works best when trying to identify cases of pulmonary embolism, hs-D Dimer assays came out on top showing an additional 25 to 30% sensitivity over some point-of-care versions. As such these findings seem indicate that in all settings but most especially among low-risk groups where there is high prevalence this particular assay should be considered as being more accurate and reliable for diagnosing VTE and DVT.

Challenge: Determining Apt Cut-off Level of D-Dimer Testing

Positive from negative results are distinguished by cutoff levels in D-dimer tests, which affects its accuracy. These levels determine the sensitivity or specificity with which true negatives and positives are detected in the D-dimer testing market. It is important to choose the correct cutoff so as not to make wrong diagnoses. The biggest problem faced is that there is no standardization among different types of D-dimer assays. Various methods used by different manufacturers cause variations whereby some studies showed a specific range between 30% and over 90%. Therefore, it becomes difficult to compare findings across laboratories.

Also, age matters too. Normally, levels of D-dimers increase with age hence using a fixed cutoff may be inappropriate for older patients. According to researches not all assays have them verified but age-adjusted cutoffs (age x 10 μg/L for over 50s) could improve specificity while still ruling out clots based on sensitivity. Similarly, the right cutoff varies depending on which specific assay you use for your patient population. One study found different cut-offs applied by various assays (0.5 mg/L FEU – 0.82 mg/L FEU). Therefore, manufacturers should validate their tests and recommend proper limits through clinical trials.

Apart from the test itself, selection of an appropriate pretest probability (clinical context and likelihood of blood clotting) greatly influences the choice of cut-off points in the D-dimer testing market. In cases where chances are low then one may go for higher values so as not to miss many positive results without necessarily affecting its sensitivity for ruling out clots. When setting a limit, one has to balance between being sensitive or specific enough because lowering it will decrease false negatives but increase false positives whereas raising it lowers false positive rates at expense of missing true ones. The best trade-off depends on situation severity if overlooked vis-à-vis unnecessary further investigations like CT scans etc., thus high sensitivities (>95%) are desirable when excluding PE.

Segmental Analysis

By Testing Method

The laboratory segment accounts for 73.92% of the D-dimer testing market. These labs are equipped with sophisticated equipment and skilled personnel who can conduct highly sensitive D-dimer assays commonly used to rule out venous thromboembolism (VTE) and manage disseminated intravascular coagulation (DIC). Physicians have become increasingly interested in quick point-of-care (POC) D-dimer assays for screening patients with suspected thromboembolic disease as urgent care facilities become more crowded and they strive for better patient satisfaction and shorter waiting times. In addition, laboratories are essential for diagnosing DIC, which involves various tests such as complete blood count (CBC) to determine platelet number, clotting factor concentration determinations, and coagulation assays that measure how long it takes blood to clot among other things; clinical labs have all these capabilities under one roof hence their usefulness in comprehensive D-dimer testing and managing complex clotting disorders.

The POC segment has the highest CAGR of 5.64% in the global D-dimer testing market. To begin with, faster results through POC testing makes patients happy because it cuts down on wait time before diagnosis is made so speed matters most here compared to other types of tests. This need alone creates a substantial demand-pull factor for point of care tests besides immediacy, there are other reasons why they continue gaining popularity; One being global rise in chronic illnesses mainly among elderly individuals thus creating more need Secondly technological advancements like next generation aptamer based microfluidic solutions enhance innovation while cutting costs at the same time. Thirdly convenience associated with access points closer home especially when dispersed healthcare settings come into play such as doctors' offices or even urgent care clinics and lastly cost effectiveness compared against lab based methods further drives adoption rates up plus overall market growth.

By Application

Deep Vein Thrombosis (DVT) holds the high share of 45.62% in the global D-dimer testing market and is projected to grow at the highest CAGR of 5.16% during the forecast period. As chronic diseases become more widespread, DVT is increasingly becoming common. This is the reason why there should be accurate diagnosis with D-dimer tests. In addition, as aging occurs globally and particularly in developed countries where most people live longer lives than ever before, this demographic, which has higher susceptibility to DVT also raises its demand level because of them. Pulmonary embolism is a life-threatening complication that can arise from deep vein thrombosis if not diagnosed early enough. It follows then that these examinations should only take between 60-90 minutes from sample collection until treatment initiation based on its high sensitivity (>95%) for detecting acute cases.

The point-of-care (POC) D-dimer testing market has been transformed by technological advancements. These new inventions provide results within minutes instead of hours or days; they are cheaper than traditional methods done in labs and can be used anywhere at any time making them very convenient especially where patients need to know their status quickly like emergency departments when excluding DVTs promptly among other disorders. Moreover, it must also be noted that ultrasound is often combined with clinical probability assessments plus imaging studies such as venous Doppler as part of diagnostic algorithms used for working up suspected deep venous thrombosis (DVT). This means that adding D-dimer into the mix would only serve to make the process faster while still maintaining safety levels required during investigation stages hence its continued integration into protocols even though it may not always completely rule out PE or other diseases found along veins during imaging evaluation.

By End User

Hospitals & clinic segment accounted for over 60.0% revenue share of the global d-dimer testing market. Hospitals are faced with Venous Thromboembolism (VTE), a condition that includes blood clots (DVT) and lung clots (PE). Up to 60% of VTE cases happen during hospitalization, affecting anywhere from 10 to 30 out of every 1,000 admissions. In the fight against VTE, D-dimer testing is an indispensable tool. The use of D-dimer tests is extensive in emergency departments (EDs) where they account for 21.3% of visits for suspected VTE. When used alongside scoring systems like the Wells score, D-dimer tests can safely eliminate VTE in between 30-50% of ED patients thus doing away with the need for unnecessary and expensive imaging tests. Intensive care units (ICUs) also employ D-dimer testing as part of their Disseminated Intravascular Coagulation (DIC) monitoring since DIC is a grave bleeding and clotting disorder. In ICU patients with levels higher than or equal to 4 mg/L, D-dimer has have a sensitivity rate of about 90% in diagnosing DIC.

The COVID-19 pandemic served to highlight the importance of D-dimer testing market even further because elevated levels thereof are associated with severe cases of COVID-19 infection. Current research indicates that persons diagnosed with severe COVID-19 showcase average elevation levels ranging from being as low as 0.54 mg/L higher than individuals suffering from milder forms. Otherwise; another separate study discovered that if admitted into hospital having levels exceeding this value then such patients would be at risk eighteen times greater than those whose measurements did not meet this criterion i.e., for dying due this disease alone. It should also be noted that among other things besides its usefulness in diagnosing aortic dissection – which is one life threatening condition -, there exists evidence proving that when incorporated into diagnostic algorithms, it can reduce time taken for making a diagnosis by 5.4 hours as well as saving up to thirteen thousand dollars per client.

Hospitals in the global D-dimer testing market can widely distribute D-dimer tests given their easy availability, quick turnaround times (less than an hour), and relatively cheap nature compared with imaging tests; thus, making them a cost-effective first-line option for excluding VTE. In actual sense; studies have shown that if used together with clinical decision rules then this could save anything from two hundred to four hundred dollars per patient through minimizing unwarranted use of imaging.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

To Understand More About this Research: Request A Free Sample

Regional Analysis

North America holds the highest market share of 35.32% in the D-dimer testing market. There is a high demand for D-dimer tests due to an increase in cardiopulmonary disorders and blood diseases like venous thromboembolism (VTE), strokes, and disseminated intravascular coagulation (DIC) among elderly people living in North America. In fact, every year, over 250,000 hospitalizations are caused by pulmonary embolism alone in the United States which contribute greatly towards increasing need for D-dimer testing. Additionally, the presence of guidelines on how to manage VTEs further drives demand for coagulation tests within different regions of North America. Another factor that played a role was introduction of automated enzyme-linked immunosorbent assay (ELISA) systems into US based companies engaged with D-dimer testing industry and it has also helped raise their market shares. Some major players in this region include but not limited to Laboratory Corporation of America Holdings; Response Biomedical Corp; Unbound Medicine Inc., Helena Laboratories etc., all these companies are actively involved in promoting growth through various measures such as new product development among others.

Asia Pacific D-dimer testing market is projected to record fastest CAGR of 5.68% during forecast period as the region has many countries like India, China, Indonesia, and the Philippines experiencing rapid population growth. Hence, creating huge demands particularly when it comes to healthcare services delivery systems including diagnosis capabilities especially relating blood clotting disorders which require use or rather application thereof d- dimer test kits. In addition, there have also been made significant advances in clinical researches assay systems installations within APAC region, especially within newly established government funded hospitals.

At same time, healthcare infrastructure continues to improve on daily basis even though much needs to be done in terms of equipping these facilities with more advanced tools necessary. This is for diagnosing a wide range of diseases including those associated with blood clotting hence making such kind tests easily accessible thus enabling early detection treatment saving many lives otherwise lost due late intervention. It is worth noting that most economies in this regional D-dimer testing market of the world are experiencing rapid growth hence leading increased expenditure towards health sector which has resulted into affordable pricing models covering larger percentage population thereby increasing affordability levels therefore creating huge market potentialities for d- dimer test kits across different regions within Asia Pacific continent.

Key Players in the Global D-dimer Testing Market

- Abbott Laboratories

- Advy Chemical Pvt. Ltd.

- BioMerieux

- Bio-Rad Laboratories Inc.

- Beckman Coulter, Inc.

- F Hoffmann-La Roche Ltd

- Henry Schein Inc.

- HyTest Ltd

- LumiraDx

- Merck KGaA

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

- Other Prominent Players

Recent Developments

- In Oct 2023, LumiraDx collaborates with AstraZeneca and Everton in the Community to establish England’s inaugural Heart & Lung Screening Hub.

- In Oct 2022, Vedalab Showcases Innovative Reagents and Instruments at MEDICA 2022

- In June 2022, LumiraDx Enhances its Cardiovascular Testing Portfolio by Securing CE Marking for its NT-proBNP Test and Introducing a New Exclusion Claim for its D-Dimer Test.

Market Segmentation Overview:

By Testing Method

- Laboratory

- Clinical Chemistry Analyzer

- Coagulation Analyzer

- Point-Of-Care

By Application

- Deep Vein Thrombosis (DVT)

- Disseminated intravascular Coagulation (DIC)

- Pulmonary Embolism (PE)

- Stroke

By End User

- Hospitals & Clinics

- Diagnostic Centers

- Research Institutions

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |